Global Veterinary Diagnostics Market Size, Share, Trends & Growth Analysis Report – Segmented By Product Type (Clinical Chemistry, Molecular Diagnostics, Hematology, Diagnostic Imaging and Immunodiagnostics), Animal and Region - Industry Forecast From 2024 to 2033

Global Veterinary Diagnostics Market Size

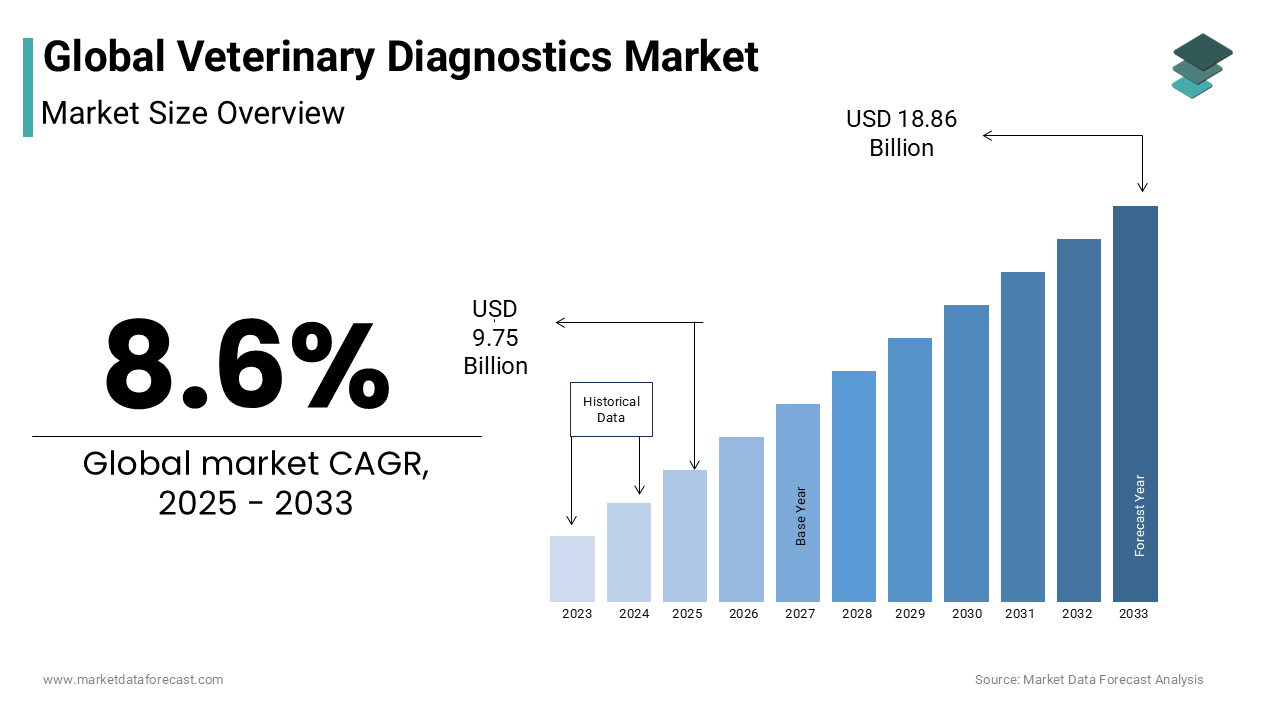

The global veterinary diagnostics market is estimated to grow from USD 8.98 billion in 2024 to USD 18.86 billion in 2033, representing a CAGR of 8.6%.

Current Scenario of the Global Veterinary Diagnostics Market

Veterinary Diagnostics refers to the tools, reagents, imaging systems, and laboratory services designed to detect, monitor, and manage diseases in animals. This domain spans companion animals, livestock, and exotic species, integrating technologies such as molecular diagnostics, immunoassays, hematology, and point-of-care testing. As animal health becomes increasingly intertwined with public health, particularly in the context of zoonotic disease surveillance and food safety, the precision and timeliness of diagnostic outcomes have assumed critical importance.

The World Organisation for Animal Health (WOAH) underscores that over 70% of emerging infectious diseases in humans originate from animals, reinforcing the necessity for robust veterinary diagnostic infrastructure. Furthermore, the rise in pet ownership, particularly in urban centers across North America and Europe, has catalyzed demand for advanced clinical diagnostics. According to the American Pet Products Association, 70% of U.S. households owned a pet in 2023, up from 56% in the early 2000s, reflecting a societal shift toward greater animal healthcare investment. These dynamics, coupled with regulatory frameworks promoting animal disease traceability and biosecurity, position veterinary diagnostics as a pivotal sector in both veterinary medicine and global health security.

MARKET DRIVERS

Increasing Prevalence of Zoonotic and Infectious Animal Diseases

The escalating incidence of zoonotic and contagious animal diseases serves as a primary catalyst for the expansion of the veterinary diagnostics market. Pathogens such as avian influenza, bovine tuberculosis, and Rift Valley fever continue to threaten animal populations and human health, necessitating rapid and accurate diagnostic interventions. This upward trend underscores the growing need for real-time surveillance and diagnostic preparedness. Also, molecular diagnostic techniques, including PCR-based assays, have become indispensable in identifying pathogen variants swiftly. As global health agencies advocate for a One Health approach, integrating animal, human, and environmental health monitoring, the reliance on advanced diagnostic platforms continues to grow, reinforcing their centrality in preventing large-scale epidemics.

Rising Pet Ownership and Humanization of Companion Animals

A transformative shift in societal attitudes toward pets, viewing them as family members rather than mere animals, has significantly amplified demand for advanced veterinary diagnostics. This humanization trend has led pet owners to seek medical care for their animals that parallels human healthcare standards, including preventive screenings, chronic disease monitoring, and geriatric diagnostics. As per the American Pet Products Association’s 2023 survey, approximately 70% of U.S. households, equating to nearly 90 million homes, own at least one pet, with dogs and cats being the most prevalent.

The surge is driven by a willingness to invest in early disease detection tools such as blood panels, urinalysis, and imaging technologies. In Japan, where the aging population increasingly adopts pets for companionship, the number of registered dogs and cats exceeded 16 million in 2023, as per the Japan Pet Food Association. Concurrently, veterinary clinics in urban centers like Tokyo and Osaka have integrated point-of-care diagnostic devices to deliver rapid results during consultations. In Europe, the European Pet Federation estimates that over 200 million pets reside across member states, with diagnostic service penetration rising steadily. The emotional and financial investment in pet well-being has thus created a sustainable demand for sophisticated diagnostic solutions, positioning the sector for long-term growth driven by consumer behavior rather than mere clinical necessity.

MARKET RESTRAINTS

Limited Access to Advanced Diagnostic Infrastructure in Developing Regions

A significant portion of the global veterinary diagnostics market remains constrained by inadequate infrastructure, particularly in low- and middle-income countries. Rural and remote veterinary practices often lack access to reliable electricity, refrigeration for reagents, and trained personnel capable of operating complex diagnostic equipment. In India, as per a 2022 study published by the Indian Council of Agricultural Research, only 28% of district veterinary hospitals were equipped with functional diagnostic laboratories, despite the country housing over 535 million livestock. This deficiency delays disease detection, exacerbates outbreaks, and undermines national control programs. Without scalable, cost-effective diagnostic platforms and sustained investment in veterinary education and infrastructure, these regions remain vulnerable to preventable disease spread, constraining the equitable growth of the global veterinary diagnostics ecosystem.

High Cost of Advanced Diagnostic Equipment and Reagents

The financial burden associated with acquiring and maintaining cutting-edge diagnostic technologies presents a formidable barrier to market penetration, especially for small and independent veterinary practices. Sophisticated instruments such as real-time PCR machines, flow cytometers, and digital radiography systems often carry acquisition costs, with additional annual expenses for calibration, software updates, and proprietary reagents. Moreover, recurring expenses for consumables and quality control materials further strain operational budgets. These economic pressures limit the scalability of advanced diagnostics, particularly in price-sensitive regions, and hinder the transition from reactive to preventive veterinary care models.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Digital Health Platforms

The convergence of artificial intelligence (AI) and digital veterinary platforms is unlocking transformative opportunities in diagnostic accuracy and operational efficiency. Machine learning algorithms are now being deployed to interpret radiographic images, analyze hematological patterns, and predict disease progression with growing reliability. Also, telemedicine platforms integrated with diagnostic data management systems are enabling remote consultations and real-time monitoring, particularly beneficial in underserved areas. Furthermore, wearable biosensors that transmit physiological data to centralized AI systems are gaining traction in equine and dairy farming. As connectivity improves and algorithmic models become more refined, AI-driven diagnostics are poised to redefine speed, precision, and accessibility across species and geographies.

Expansion of Point-of-Care Testing in Field and Clinical Settings

The evolution of portable, rapid, and user-friendly diagnostic devices is creating substantial growth potential, particularly in field applications and primary care clinics. Point-of-care (POC) testing enables immediate results for conditions such as heartworm, feline leukemia, and glucose monitoring, facilitating prompt treatment decisions without reliance on centralized labs. In disaster response scenarios, such as the 2023 floods in Pakistan, field-deployable PCR units enabled rapid screening of leptospirosis in displaced livestock populations, preventing wider zoonotic transmission. With ongoing miniaturization, improved sensitivity, and decreasing costs, POC diagnostics are transitioning from niche tools to mainstream components of veterinary practice, offering scalable solutions for both companion and production animals.

MARKET CHALLENGES

Regulatory Fragmentation and Standardization Gaps in Diagnostic Validation

A persistent challenge in the veterinary diagnostics market is the absence of harmonized global regulatory standards for test validation, approval, and post-market surveillance. Unlike human diagnostics, which are governed by stringent frameworks such as the U.S. FDA’s 510(k) or the EU’s IVDR, veterinary assays often face inconsistent approval pathways across jurisdictions. In India, the lack of a centralized approval mechanism means that many commercially available ELISA kits enter the market without independent performance verification, leading to variability in sensitivity and specificity. Similarly, in Latin America, regulatory oversight varies widely; while Brazil’s Ministry of Agriculture enforces rigorous validation protocols, neighboring countries often rely on imported tests without local verification. This fragmentation undermines diagnostic reliability, complicates international trade in animal products, and erodes trust among veterinarians and producers. Without a unified global framework for performance standards and quality control, the risk of misdiagnosis and disease spread remains elevated, impeding the credibility and scalability of innovative diagnostic solutions.

Shortage of Skilled Veterinary Diagnosticians and Technical Personnel

The global veterinary diagnostics sector faces a critical deficit in trained professionals capable of interpreting complex test results and managing advanced instrumentation. While technological capabilities have advanced rapidly, workforce development has not kept pace, particularly in molecular diagnostics, cytology, and bioinformatics. In the United States, the American Society for Veterinary Clinical Pathology reported in 2023 that only 320 board-certified clinical pathologists were actively practicing, insufficient to meet the demands of over 100,000 veterinary clinics. This scarcity is exacerbated in rural and resource-limited settings, where veterinarians often assume multiple roles without access to mentorship or continuing education. The skills gap extends to data interpretation, where the integration of genomic and proteomic diagnostics requires expertise in bioinformatics. Without targeted investments in education, certification, and professional development, the full potential of advanced diagnostics will remain unrealized, constraining both clinical outcomes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Product, Animal, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Qiagen N.V., Zoetis Inc., IDEXX Laboratories, Inc. and Heska Corporation, VCA Inc., Abaxis, Inc., VIRBAC, Life Technologies Corporation, Bio-Rad Laboratories Inc., Prionics AG, and Pfizer, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The immunodiagnostics segment held the largest market share at accounting for a 34.5% in 2024. This dominance is primarily driven by the widespread application of immunoassay-based tests, such as ELISA, lateral flow assays, and rapid antigen detection kits, in diagnosing infectious diseases across both companion and food-producing animals. One of the principal drivers of this segment’s position is the escalating demand for point-of-care (POC) infectious disease testing, particularly for conditions like feline leukemia, canine parvovirus, and bovine viral diarrhea. The high sensitivity, cost-effectiveness, and ease of use of these assays make them ideal for decentralized testing environments. These operational advantages, combined with rising zoonotic disease threats and regulatory emphasis on early pathogen detection, continue to solidify immunodiagnostics as the cornerstone of modern veterinary laboratory practice.

The molecular diagnostics segment is expanding at the fastest pace in the veterinary diagnostics market and is recording a CAGR of 12.8% between 2025 and 2033. This accelerated growth is fueled by the increasing need for high-precision pathogen identification and genetic disease screening, particularly in specialized veterinary care and biosecurity programs. A key driver is the rising adoption of polymerase chain reaction (PCR) and next-generation sequencing (NGS) technologies in clinical settings. A further critical factor is the expansion of genetic testing for inherited disorders in purebred animals. Furthermore, portable PCR devices like the Biomeme two3 system have enabled field-deployable molecular testing. With increasing investments in veterinary genomics and antimicrobial resistance profiling, molecular diagnostics is transitioning from a niche specialty to a mainstream clinical tool, propelling its market leadership in growth trajectory.

By Animal Insights

The companion animals segment dominated the veterinary diagnostics market by capturing 55.3% of total revenue in 2024. This preeminence stems from a confluence of socio-economic and behavioral shifts that have elevated the status of pets within households, particularly in high-income nations. The deepening emotional and financial investment in pet health, often mirroring human healthcare expectations, is a primary driver. This trend is reinforced by the aging pet population. Besides, the integration of wellness plans and pet insurance, covering diagnostic testing, has reduced financial barriers to care. These factors collectively sustain robust demand for advanced diagnostics in companion animal medicine, ensuring its continued market dominance.

The food-producing animals segment is emerging as the fastest-growing category in the veterinary diagnostics market and is projected to expand at a CAGR of 10.4% from 2025 to 2033. This surge is primarily driven by intensifying global food safety regulations and the economic imperative to safeguard livestock productivity. With animal-source proteins remaining central to global nutrition, early disease detection has become critical to minimizing production losses and trade disruptions. In India, the National Animal Disease Control Programme (NADCP) allocated ₹13,343 crore (approximately $1.6 billion) between 2019 and 2024 to eradicate foot-and-mouth disease and brucellosis through mass screening, resulting in over 200 million diagnostic tests administered by 2023. A different pivotal factor is the rise of large-scale commercial farming, particularly in Asia and Latin America. Furthermore, the European Union’s 2022 Animal Health Law mandates compulsory diagnostic monitoring for diseases such as bovine tuberculosis and African swine fever, significantly increasing test volume across member states. With growing pressure to ensure antibiotic stewardship and prevent zoonotic spillover, the integration of diagnostics into livestock management systems is accelerating, positioning this segment for sustained high-growth momentum.

REGIONAL ANALYSIS

North America Veterinary Diagnostics Market Insights

North America maintained a commanding position in the global veterinary diagnostics market by securing a 42.5% share in 2024. The region’s place is anchored in its highly developed veterinary healthcare infrastructure, widespread pet insurance penetration, and strong regulatory support for animal disease surveillance. Additionally, federal initiatives such as the USDA’s National Animal Health Laboratory Network (NAHLN), comprising 60+ laboratories, facilitate rapid response to disease outbreaks. High consumer willingness to pay—evidenced by $35.9 billion in annual veterinary expenditures—is further amplified by the presence of leading diagnostic firms such as IDEXX Laboratories and Zoetis, headquartered in Maine and New Jersey, respectively. These structural advantages ensure North America’s continued dominance in innovation, adoption, and market value.

Europe Veterinary Diagnostics Market Insights

Europe holds a strong position in the global veterinary diagnostics market. The region’s market maturity is underpinned by stringent animal health regulations, a dense network of veterinary professionals, and a strong emphasis on food safety and zoonotic disease control. Germany, France, and the United Kingdom collectively account for a key share of Europe’s diagnostic revenue, driven by high pet ownership rates and advanced livestock monitoring systems. The European Medicines Agency (EMA) and EFSA jointly oversee antimicrobial use and disease reporting, mandating diagnostic confirmation for notifiable diseases such as avian influenza and rabies. With increasing investment in digital veterinary platforms and AI-assisted diagnostics, Europe remains a hub of regulatory innovation and clinical excellence in veterinary medicine.

Asia-Pacific (APAC) Veterinary Diagnostics Market Insights

The Asia-Pacific region is rapidly ascending as a pivotal force in the veterinary diagnostics landscape. While historically behind North America and Europe in diagnostic adoption, APAC is experiencing accelerated growth due to rising pet ownership, government-led disease eradication programs, and expanding commercial livestock operations. China and India are the primary growth engines. In India, the National Animal Disease Control Programme conducted over 200 million serological tests for foot-and-mouth disease and brucellosis between 2019 and 2023, creating massive demand for ELISA and rapid kits. Australia, a regional leader in regulatory standards, mandates diagnostic testing for export livestock. Additionally, Japan’s aging population has driven pet humanization trends, with diagnostic imaging and genetic testing becoming commonplace in Tokyo’s veterinary clinics. With increasing foreign investment and technology transfer, APAC is transitioning from a price-sensitive market to a center of diagnostic innovation and volume.

Latin America Veterinary Diagnostics Market Insights

Latin America holds a significant share of the global veterinary diagnostics market, with Brazil and Mexico leading regional demand. The region’s market dynamics are shaped by its vast livestock economy and growing awareness of animal health’s role in international trade. Brazil, the world’s largest exporter of beef and poultry, conducts a substantial number of diagnostic tests annually to comply with import regulations from the EU and China. Mexico’s National Service for Agrifood Health, Safety, and Quality (SENASICA) implemented a nationwide brucellosis eradication program, administering millions of diagnostic tests in 2022 alone. However, access remains uneven. Despite these challenges, private-sector growth is evident, Chile’s pet diagnostic market has expanded in recent times, driven by rising urban pet ownership. Additionally, partnerships with global firms like IDEXX and Thermo Fisher have enhanced reagent availability and training. While infrastructure gaps persist, Latin America’s economic reliance on animal agriculture ensures sustained momentum in diagnostic adoption.

Middle East and Africa Veterinary Diagnostics Market Insights

The Middle East and Africa collectively account for a small share of the global veterinary diagnostics market, with significant variation across subregions. Gulf Cooperation Council (GCC) countries such as the United Arab Emirates and Saudi Arabia are driving market modernization, fueled by rising pet ownership and luxury animal care. In contrast, Sub-Saharan Africa’s market remains constrained by infrastructure deficits, yet exhibits strategic growth in disease surveillance. South Africa stands out with a developed veterinary network. Despite challenges, regional initiatives and increasing public-private partnerships are laying the foundation for long-term diagnostic expansion..

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Qiagen N.V., Zoetis Inc., IDEXX Laboratories, Inc., and Heska Corporation play a leading role in the global veterinary diagnostics market. Other notable companies active in the market are VCA Inc., Abaxis, Inc., VIRBAC, Life Technologies Corporation, Bio-Rad Laboratories Inc., Prionics AG and Pfizer, Inc. are a few of the prominent companies in the global veterinary diagnostics market.

The competition in the veterinary diagnostics market is intensifying as established players and emerging innovators vie for technological leadership and geographic dominance. The sector is characterized by a blend of large multinational corporations with integrated portfolios and agile startups specializing in AI-driven diagnostics, wearable biosensors, and molecular detection platforms. Incumbents such as IDEXX Laboratories, Zoetis, and Thermo Fisher Scientific leverage their extensive distribution networks, regulatory expertise, and strong brand recognition to maintain influence across both companion and food-producing animal segments. However, they face growing pressure from specialized firms offering cost-effective, rapid, and decentralized testing solutions tailored to resource-limited settings. Competitive differentiation is increasingly achieved through digital integration, where diagnostic devices are linked to cloud-based software for real-time data interpretation and clinical decision support. Mergers, acquisitions, and strategic collaborations are common as companies seek to enhance their technological capabilities and expand into high-growth regions. Regulatory alignment, speed to market, and adaptability to local disease profiles are critical success factors. Moreover, the rise of antimicrobial resistance and zoonotic threats has elevated the strategic importance of veterinary diagnostics in global health security, attracting investment and innovation. As demand for precision medicine in animals grows, the competitive landscape is evolving from product-centric offerings to comprehensive health ecosystems that combine diagnostics, therapeutics, and data analytics.

Top Players in the Veterinary Diagnostics Market

IDEXX Laboratories, Inc.

IDEXX Laboratories has established a dominant presence in the Asia Pacific veterinary diagnostics market through its comprehensive portfolio of point-of-care instruments, reference laboratory services, and cloud-based practice management software. The company’s Catalyst One chemistry analyzers and SNAP testing platforms are widely adopted across private clinics in Australia, Japan, and South Korea, where demand for rapid, in-clinic diagnostics continues to rise. The company has also invested in localized customer support and training programs in India and Indonesia, partnering with veterinary universities to improve test utilization. IDEXX’s integration of its Cornerstone practice management software with diagnostic devices enables seamless data flow, a feature increasingly valued by tech-forward clinics. Additionally, the firm strengthened its infectious disease testing capabilities by introducing region-specific ELISA kits for bovine and avian pathogens, aligning with government-led livestock health initiatives. These strategic moves underscore IDEXX’s commitment to delivering scalable, high-precision diagnostic solutions tailored to the diverse needs of the Asia Pacific region.

Zoetis Inc

Zoetis has emerged as a pivotal player in the Asia Pacific veterinary diagnostics landscape by combining its pharmaceutical expertise with a growing suite of diagnostic tools designed to support integrated animal health management. The company’s DRI-CHEM 7000 analyzer and SNAP Leishmania test are extensively used in companion animal clinics across Japan, Australia, and New Zealand, where veterinarians emphasize preventive care and early disease detection. The company also collaborated with Thailand’s Department of Livestock Development to deploy rapid antigen tests for foot-and-mouth disease, supporting national eradication efforts. Zoetis has further deepened its engagement through educational initiatives, sponsoring diagnostic workshops for veterinarians in Vietnam and the Philippines. By aligning its diagnostic offerings with vaccine and therapeutic portfolios, Zoetis enhances treatment adherence and strengthens client loyalty. Its focus on innovation and public-private partnerships enables the company to address both clinical and regulatory demands, solidifying its role as a comprehensive health solutions provider across the Asia Pacific region.

Thermo Fisher Scientific Inc

Thermo Fisher Scientific plays a critical role in the Asia Pacific veterinary diagnostics market by supplying high-end analytical instruments, molecular testing reagents, and laboratory automation systems to reference labs, research institutions, and government agencies. Its real-time PCR platforms, such as the Applied Biosystems QuantStudio series, are widely deployed in national animal health laboratories across Australia, South Korea, and Malaysia for pathogen surveillance and antimicrobial resistance monitoring. The company also introduced a localized version of its TaqMan assays for avian influenza and African swine fever, optimized for regional virus strains. Collaborating with the Australian Animal Health Laboratory (AAHL), Thermo Fisher supported genomic sequencing efforts during the 2022–2023 lumpy skin disease outbreaks in Southeast Asia. Furthermore, its partnership with India’s National Institute of High Security Animal Diseases (NIHSAD) strengthened diagnostic capacity for transboundary diseases. Through technology transfer, training programs, and regulatory alignment, Thermo Fisher Scientific continues to empower laboratories across the region with scalable, precision-driven diagnostic infrastructure.

Top Strategies Used by the Key Market Participants

Key players in the veterinary diagnostics market are deploying a range of strategic initiatives to consolidate their positions and drive innovation. Major strategies include product innovation, geographic expansion, strategic partnerships, acquisitions, and digital integration. Companies are increasingly investing in the development of rapid, portable, and multiplex diagnostic platforms that enable point-of-care testing in both clinical and field settings. Geographic expansion is particularly pronounced in emerging markets such as India, Indonesia, and Brazil, where rising pet ownership and government disease control programs are creating new demand. Firms are forming alliances with veterinary schools, government agencies, and agricultural cooperatives to enhance market penetration and build trust. Acquisitions of niche technology developers allow larger companies to integrate novel detection methods, such as CRISPR-based assays or AI-powered imaging analysis. Digital integration is another critical focus, with companies linking diagnostic devices to cloud-based platforms for data analytics, remote monitoring, and electronic health record synchronization. These strategies are designed to improve diagnostic accuracy, reduce turnaround time, and increase user dependency on proprietary ecosystems. Additionally, regulatory compliance and localization of test kits for regional pathogens are being prioritized to meet diverse market requirements. Collectively, these approaches enable market leaders to maintain technological leadership, expand customer reach, and respond dynamically to evolving animal health challenges across species and geographies.

RECENT MARKET HAPPENINGS

-

In January 2023, IDEXX Laboratories launched a new veterinary reference laboratory in Singapore to enhance diagnostic testing capacity and reduce turnaround times for clinics across Southeast Asia, supporting regional expansion and service reliability.

In May 2023, Zoetis partnered with Thailand’s Department of Livestock Development to deploy rapid antigen tests for foot-and-mouth disease, strengthening national surveillance and reinforcing its role in public-sector animal health programs.

-

In September 2023, Thermo Fisher Scientific introduced region-specific TaqMan assays for avian influenza and African swine fever in India and Vietnam, improving pathogen detection accuracy and aligning with local outbreak control initiatives.

-

In November 2023, Heska Corporation expanded its distribution network in Australia and New Zealand by collaborating with local veterinary distributors to increase access to its AccuTrol quality control products and diagnostic analyzers.

-

In February 2024, bioMérieux launched a mobile training unit in Kenya to educate veterinarians on the use of its VITEK MS mass spectrometry system for microbial identification, enhancing technical adoption in emerging markets.

MARKET SEGMENTATION

This research report on the global veterinary diagnostics market has been segmented and sub-segmented based on animals, products, and regions.

By Product

- Clinical Chemistry

- Urine Analysis

- Glucose Monitoring

- Blood Gas Electrolyte Analysis

- Molecular Diagnostics

- Micro Arrays

- PCR Tests

- Other Molecular Diagnostics Tests

- Hematology

- Hematology Analysers

- Hematology Cartridges

- Diagnostic Imaging

- Radiography Systems

- Ultrasound Imaging Systems

- CT Scanners

- MRI Scanners

- Immunodiagnostics

- Immunoassay Analysers

- ELISA Tests

- Lateral-Flow Strip Readers

- Lateral-Flow Rapid Tests

- Allergen-specific Immunodiagnostic Tests

By Animal

- Companion Animals

- Canine Diagnostics

- Feline Diagnostics

- Other Veterinary Diagnostics

- Food-Producing Animals

- Bovine Diagnostics

- Porcine Diagnostics

- Ovine Diagnostics

- Poultry Diagnostics

- Piscine Diagnostics

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What was the size of the veterinary diagnostics market worldwide in 2023?

The global veterinary diagnostics market size was valued at USD 8.27 billion in 2023.

Does this report include the impact of COVID-19 on the veterinary diagnostics market?

Yes, we have studied and included the COVID-19 impact on the global veterinary diagnostics market in this report.

Which region is anticipated to witness fastest growth in the veterinary diagnostics market?

During the forecast period, the Asia-Pacific region is anticipated to grow at the fastest CAGR in the worldwide market.

Who are the key players in the global veterinary diagnostics market?

Qiagen N.V., ZoetisInc., IDEXX Laboratories, Inc., Heska Corporation, VCA Inc., Abaxis, Inc., VIRBAC, Life Technologies Corporation, Bio-Rad Laboratories Inc., Prionics AG, and Pfizer, Inc. are some of the notable companies in the veterinary diagnostics market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com