Europe Optical Transceiver Market Size, Share, Trends & Growth Forecast Report – Segmented By Form Factor, Data Rate, Fiber Type, Distance, Wavelength, Connector, Protocol, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Optical Transceiver Market Report Summary

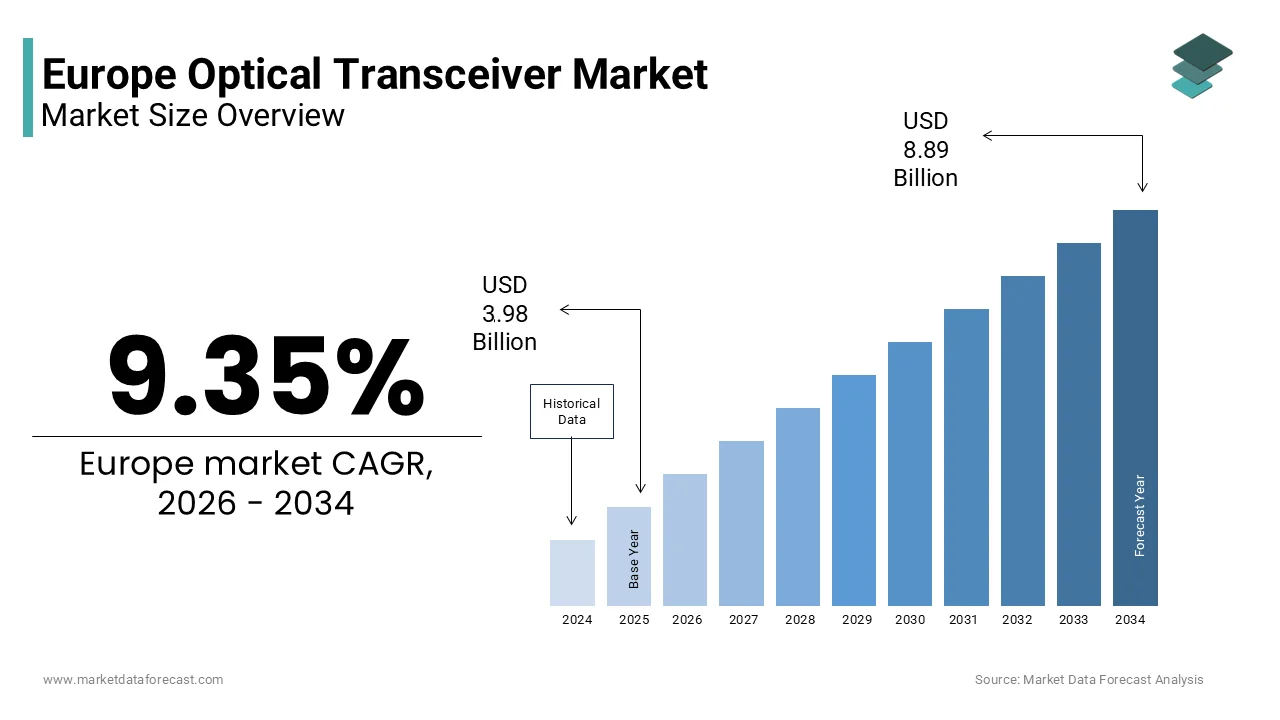

The Europe optical transceiver market was valued at USD 3.98 billion in 2025 and is estimated to reach USD 4.35 billion in 2026, and is projected to reach USD 8.89 billion by 2034, growing at a CAGR of 9.35% during the forecast period. The growth of the Europe optical transceiver market is driven by the rapid expansion of high speed communication networks, increasing deployment of 5G infrastructure, and the growing demand for data center connectivity across the region. Rising internet traffic, cloud computing adoption, and large scale digital transformation initiatives are encouraging telecom operators and enterprises to upgrade network infrastructure with high performance optical components. In addition, the increasing need for faster data transmission, low latency connectivity, and scalable network solutions is further accelerating the adoption of optical transceivers in Europe.

Key Market Trends

- Growing deployment of 5G networks across Europe increasing demand for high speed optical transceivers to support advanced mobile communication infrastructure.

- Rising investments in hyperscale data centers and cloud services boosting the adoption of optical interconnect technologies.

- Increasing demand for high bandwidth connectivity driven by expanding internet traffic, video streaming, and enterprise digitalization.

- Advancements in optical communication technologies enabling higher data transmission speeds and improved network efficiency.

- Expansion of fiber based communication infrastructure across European countries supporting the growth of optical networking components.

Segmental Insights

- Based on form factor, the SFP Plus and SFP28 segment accounted for 42.6% of the Europe optical transceiver market share in 2025. The strong adoption of these form factors is attributed to their compact design, high speed data transmission capability, and wide compatibility with networking equipment used in telecom and data center environments.

- Based on fiber type, the single mode fiber based optical transceivers segment held the largest share of the Europe optical transceiver market in 2025. The segment’s dominance is driven by its ability to support long distance communication with minimal signal attenuation, making it highly suitable for telecom backbone networks and large scale data transmission applications.

Regional Insights

- The Europe optical transceiver market is experiencing steady growth across several countries supported by increasing investments in telecommunications infrastructure and digital connectivity.

- Germany was the leading contributor to the Europe optical transceiver market, accounting for 24.3% of the market share in 2025. The country’s strong position is supported by advanced telecom infrastructure, rising data center investments, and increasing demand for high speed communication networks from enterprises and service providers.

- Other European countries are also expanding high capacity network infrastructure to support digital transformation, cloud computing, and next generation communication technologies.

Competitive Landscape

The Europe optical transceiver market is highly competitive with the presence of several global technology providers focusing on product innovation, network performance improvements, and strategic partnerships with telecom operators and data center providers. Companies are investing in advanced optical technologies to support higher data rates, energy efficient networking solutions, and scalable communication systems. Expansion of production capabilities and continuous research and development activities are enabling market players to strengthen their position in the European optical networking ecosystem. Key companies operating in the Europe optical transceiver market include Accelink Technologies, Lumentum, Innolight, Sumitomo Electric Industries Ltd, Coherent Corp, Cisco Systems Inc, Broadcom Inc, Intel Corp, and Fujitsu Ltd.

Europe Optical Transceiver Market Size

The Europe optical transceiver market size was valued at USD 3.98 billion in 2025 and is projected to reach USD 8.89 billion by 2034 from USD 4.35 billion in 2026, growing at a CAGR of 9.35%.

The optical transceiver is an electro optical device that convert electrical signals into light pulses and vice versa, serving as interface components within fiber optic communication networks, across telecommunications infrastructure, data centers, and enterprise systems. These modules enable high speed data transmission by facilitating seamless connectivity between network equipment and optical fiber cables, forming the technological foundation for modern digital ecosystems. The strategic relevance of optical transceivers has intensified as European nations advance their digital infrastructure to support bandwidth intensive applications ranging from artificial intelligence workloads to immersive media experiences. As per the European Commission, the Digital Decade initiative targets universal gigabit connectivity by 2030 by creating substantial demand for advanced optical components capable of supporting next generation network architectures. According to Eurostat, internet usage among European households reached 91% in recent measurements, reflecting widespread digital adoption that necessitates robust optical networking solutions. Furthermore, the European Investment Bank has allocated significant funding toward digital infrastructure projects, emphasizing the importance of reliable high capacity connectivity for economic competitiveness. The transition toward coherent optical technologies and silicon photonics represents a fundamental shift in transceiver design, enabling higher data rates while reducing power consumption per transmitted bit.

MARKET DRIVERS

Surging Data Center Modernization and Hyperscale Infrastructure Expansion

The accelerating modernization of data center facilities, driven by escalating demands for higher bandwidth and lower latency connectivity is escalating the growth of Europe optical transceiver market. Hyperscale operators are deploying advanced optical modules to support rack scale architectures and distributed computing environments that require seamless inter server communication. As per the International Data Corporation, European data center capacity is projected to expand by over 35% through 2027, with new facilities increasingly specifying 400 gigabit and 800 gigabit optical transceivers to handle massive east west traffic flows. The migration toward disaggregated infrastructure models necessitates dense optical interconnect solutions that can maintain signal integrity across complex topologies while minimizing power consumption per transmitted bit. Telecommunications providers are simultaneously upgrading their core networks to support cloud native services, creating parallel demand for long haul coherent transceivers capable of transmitting data over extended distances without regeneration. The European Union emphasis on data localization and digital sovereignty further accelerates investments in domestic data center infrastructure, ensuring sustained procurement of high performance optical components. Industry analysts note that power efficiency has become a decisive selection criterion, prompting manufacturers to develop transceivers with advanced thermal management and low power digital signal processors.

Accelerated Deployment of Fifth Generation Mobile Networks and Edge Computing

The widespread rollout of fifth generation mobile infrastructure, as these networks demand unprecedented fronthaul and backhaul connectivity capabilities is also elevating the growth of Europe optical transceiver market. Mobile network operators are deploying dense small cell architectures that require high-capacity optical links to connect radio units with distributed baseband processing resources. As per the study, European 5G subscriptions are expected to surpass 300 million by 2027, necessitating substantial investments in optical transport networks capable of supporting ultra reliable low latency communication services. The integration of edge computing nodes within mobile infrastructure further amplifies demand for compact, energy efficient transceivers that can operate in diverse environmental conditions while maintaining strict performance standards. Network virtualization and network function virtualization initiatives require flexible optical interfaces that can adapt to dynamic traffic patterns and service level agreements across multi vendor ecosystems. According to the European Telecommunications Standards Institute, the migration toward open radio access network architectures introduces new requirements for interoperable optical components that support standardized interfaces and management protocols. This technological evolution creates opportunities for transceiver manufacturers to develop specialized solutions optimized for mobile transport applications, including enhanced synchronization capabilities and advanced monitoring features.

MARKET RESTRAINTS

Elevated Capital Expenditure Requirements for Legacy Infrastructure Upgrades

The substantial financial burden associated with upgrading legacy fiber optic infrastructure is limiting the growth of Europe optical transceiver market. Telecommunications operators and enterprise network managers face difficult investment decisions when evaluating the cost benefit of replacing existing optical modules with higher performance alternatives. As per the Body of European Regulators for Electronic Communications, upgrading from legacy 10 gigabit transceivers to 400 gigabit coherent optics can require capital expenditures exceeding 75000 euros per network node in dense urban environments, creating financial barriers for smaller operators and public sector entities. Regulatory frameworks in several European nations impose wholesale price caps that constrain operators ability to recover infrastructure investments through service pricing, extending the operational lifespan of older optical components. The complexity of integrating advanced transceivers with heterogeneous network equipment further increases deployment costs, as operators must invest in specialized testing equipment and technical training programs.

Supply Chain Vulnerabilities and Geopolitical Dependencies for Critical Components

The supply chain vulnerabilities and dependencies on non-European sources for semiconductor and photonic components is additionally degrading the growth of Europe optical transceiver market. Manufacturing advanced optical modules requires specialized materials including indium phosphide substrates, gallium arsenide lasers, and high precision optical assemblies that are predominantly produced in Asia and North America. As per the European Semiconductor Industry Association, over 80% of the photonic integrated circuits used in European optical transceivers originate from external suppliers, creating exposure to trade restrictions, logistics disruptions, and geopolitical tensions. Recent global events have highlighted the risks associated with concentrated supply chains, prompting European policymakers to emphasize strategic autonomy in critical technology sectors. According to the European Commission, the Chips Act initiative aims to increase domestic semiconductor production capacity, but photonic component manufacturing requires specialized expertise and infrastructure that cannot be rapidly scaled. The lead times for custom optical transceivers can extend beyond 20 weeks during periods of high demand, complicating network deployment schedules and increasing inventory carrying costs for operators. This supply chain fragility limits the ability of European optical transceiver manufacturers to respond agilely to market opportunities and may constrain innovation cycles as companies prioritize supply security over technological advancement.

MARKET OPPORTUNITIES

Integration of Silicon Photonics and Coherent Technologies for Next Generation Networks

The emergence of silicon photonics and coherent optical technologies by enabling unprecedented performance improvements, while reducing manufacturing costs through semiconductor compatible processes is creating new opportunities for the growth of Europe optical transceiver market. Silicon photonics leverages established complementary metal oxide semiconductor fabrication techniques to integrate optical and electronic functions on a single chip, facilitating mass production of high performance transceivers at competitive price points. As per the European Photonics Industry Consortium, silicon photonic transceivers can achieve power consumption reductions of up to 40% compared to traditional discrete component designs, addressing critical energy efficiency requirements for sustainable data center operations. The adoption of coherent detection techniques allows optical modules to transmit data over longer distances with higher spectral efficiency, supporting the bandwidth demands of artificial intelligence training clusters and real time analytics platforms. The modular nature of silicon photonic platforms enables rapid customization for diverse application requirements, from short reach data center interconnects to long haul telecommunications links. This technological evolution positions European optical transceiver suppliers to capture value in high growth segments while contributing to the region leadership in photonic innovation and digital infrastructure development.

Expansion of Optical Transceiver Applications in Industrial Internet of Things and Smart Infrastructure

The proliferation of industrial Internet of Things deployments and smart infrastructure initiatives for optical transceiver manufacturers to address emerging application requirements is additionally to escalate new opportunities for the growth of Europe optical transceiver market. Manufacturing facilities, transportation systems, and utility networks are increasingly adopting fiber optic connectivity to support real time monitoring, predictive maintenance, and automated control functions that demand reliable high bandwidth communication. As per the European Commission Industry 5.0 framework, industrial environments require ruggedized optical components capable of operating in challenging conditions including extreme temperatures, electromagnetic interference, and mechanical vibration. Optical transceivers designed for industrial applications incorporate enhanced protection features and extended temperature ranges while maintaining the performance characteristics necessary for time sensitive networking protocols. Smart city initiatives further amplify this opportunity, as municipalities deploy fiber optic sensors and communication networks to optimize traffic management, energy distribution, and public safety services. The convergence of operational technology and information technology in industrial settings necessitates optical transceivers that support deterministic latency, precise synchronization, and robust security features.

MARKET CHALLENGES

Intensifying Competition from Alternative Connectivity Technologies and Wireless Solutions

The escalating competitive pressure from alternative connectivity technologies that offer viable substitutes for fiber optic solutions in specific application scenarios is specifically a challenge for the growth of Europe optical transceiver market. Advanced wireless technologies including millimeter wave communications and fixed wireless access have achieved performance improvements that challenge optical fiber dominance in last mile and enterprise connectivity segments. As per the European Conference of Postal and Telecommunications Administrations, fixed wireless access deployments utilizing spectrum above 24 gigahertz can now deliver multi gigabit speeds with lower deployment costs compared to fiber trenching in certain urban and suburban environments. The emergence of low earth orbit satellite constellations further expands connectivity options for remote locations where fiber infrastructure deployment faces geographical or economic constraints. According to industry analyses, the total cost of ownership for wireless solutions can be 30 to 50% lower than fiber based alternatives in low density areas, influencing operator investment decisions and potentially limiting optical transceiver addressable market expansion. Telecommunications providers are increasingly adopting hybrid network architectures that combine optical and wireless technologies to optimize coverage and capacity, reducing exclusive reliance on fiber optic infrastructure.

Complexity of Standardization and Interoperability Requirements Across Heterogeneous Network Environments

The increasing complexity of standardization and interoperability requirements optical transceiver manufacturers operating in the diverse and fragmented is also to restrict the growth of the Europe optical transceiver market. Network operators deploy equipment from multiple vendors across heterogeneous environments, necessitating optical modules that comply with evolving industry specifications while maintaining seamless compatibility with existing infrastructure. As per the European Telecommunications Standards Institute, the proliferation of multi source agreements and proprietary implementations creates integration challenges that can delay deployment timelines and increase testing overhead for optical transceiver qualification. The transition toward open radio access network architectures introduces additional complexity, as operators seek optical components that support standardized interfaces while accommodating vendor specific performance optimizations. According to industry working groups, achieving interoperability across 400 gigabit and 800 gigabit optical modules requires extensive conformance testing and field validation that can extend product development cycles and increase time to market. Regulatory requirements regarding electromagnetic compatibility, safety certifications, and environmental compliance further complicate product design and certification processes across different European jurisdictions. Manufacturers must invest substantial resources in standards participation, interoperability testing, and certification management to ensure their optical transceivers meet the diverse requirements of European network operators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.35% |

| Segments Covered | By Form Factor, Data Rate, Fiber Type, Distance, Wavelength, Connector, Protocol, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Accelink Technologies, Lumentum, Innolight, Sumitomo Electric Industries Ltd, Coherent Corp, Cisco Systems Inc, Broadcom Inc, Intel Corp, and Fujitsu Ltd |

SEGMENTAL ANALYSIS

By Form Factor Insights

The SFP Plus and SFP28 form factor segment was accounted in holding 42.6% of the Europe optical transceiver market share in 2025. The exceptional versatility of SFP Plus and SFP28 transceivers across multiple network architectures is amplifying the growth of the segment. These modules support data rates ranging from 10 gigabits per second to 28 gigabits per second, enabling seamless integration in legacy infrastructure upgrades and next generation deployments without requiring complete hardware replacement. The ability to interchange optics for different reach requirements, from short range multimode connections to long range single mode links, provides network designers with unprecedented flexibility in topology planning. Telecommunications operators leverage this adaptability to standardize inventory across access, aggregation, and core network layers, reducing operational complexity and procurement costs. Furthermore, the compact form factor enables high port density in space constrained environments such as cell tower baseband units and industrial control cabinets. This universal applicability across vertical sectors including finance, healthcare, manufacturing, and public administration ensures sustained demand regardless of specific application requirements.

The SFP Plus and SFP28 segment is projected to register a fastest CAGR of 13.7% fromk 2026 to 2034. The rapid expansion of edge computing facilities is prompting the growth of the segment. Edge data centers require compact, energy efficient optical modules that can operate in diverse environmental conditions while supporting low latency communication between distributed compute resources and central cloud platforms. As per the International Data Corporation, the number of edge computing locations in Europe is expected to increase by over 200% through 2027, with each facility typically deploying hundreds of SFP Plus or SFP28 modules for server to switch and switch to uplink connectivity. The modular nature of these transceivers enables network architects to customize optical reach and performance characteristics based on specific edge deployment requirements, from industrial facilities to retail locations and smart city infrastructure. Telecommunications operators integrating edge computing into their 5G networks rely on SFP28 optics to connect distributed units with centralized baseband processing, ensuring stringent latency requirements for applications such as autonomous vehicles and augmented reality are met. The ability to hot swap modules without disrupting network operations further enhances their appeal for edge environments where maintenance access may be limited.

By Fiber Type Insights

The single mode fiber based optical transceivers segment was the largest by capturing a significant share of the Europe optical transceiver market in 2025. Single mode fiber utilizes a core diameter of approximately 9 micrometers that enables light to propagate in a single path, virtually eliminating modal dispersion and supporting transmission distances exceeding 80 kilometers without signal regeneration. Telecommunications operators prioritize single mode optics for 5G backhaul applications where base stations must connect to core networks over extended distances while maintaining strict latency and reliability standards. Data center operators likewise leverage single mode transceivers for inter facility connections that span metropolitan areas, enabling geographic redundancy and load balancing across distributed cloud infrastructure. The future proof nature of single mode fiber, which can be upgraded to higher data rates through terminal equipment changes without replacing the cable plant, provides compelling economic advantages that reinforce its selection for new deployments.

The multimode fiber based optical transceivers segment is anticipated to grow at a fastest CAGR of 10.4% in coming years. The compelling cost benefits and installation simplicity of multimode fiber optical transceivers drive their accelerated growth in European data center environments, where connections typically span less than 500 meters. Multimode transceivers utilize larger core fibers that enable less precise alignment tolerances, reducing manufacturing costs and simplifying field termination compared to single mode alternatives. The availability of OM4 and OM5 multimode fiber standards supports data rates up to 100 gigabits per second over distances sufficient for most intra data center applications, satisfying performance requirements while maintaining economic advantages. The plug and play nature of multimode connectivity reduces deployment time and technical expertise requirements, enabling faster network expansions and modifications in dynamic cloud computing environments. European colocation providers and hyperscale operators increasingly leverage multimode optics for rack level and row level interconnects, reserving single mode technology for longer reach applications between facilities.

REGIONAL ANALYSIS

Germany Optical Transceivers Market Analysis

Germany was the top performer of the Europe optical transceivers market by holding 24.3% of the share in 2025. The robust demand across telecommunications, cloud services, and manufacturing sectors that require high performance optical connectivity to support Industry 4.0 applications. As per the German Federal Statistical Office, the country hosts over 50 hyperscale and colocation data center facilities, with Frankfurt serving as one of the world most important internet exchange points handling substantial volumes of European internet traffic. This concentration of digital infrastructure creates sustained procurement of optical transceivers for server interconnects, storage area networks, and backbone transport systems. The automotive and industrial machinery sectors, which form the backbone of the German economy, increasingly adopt fiber optic networks to enable real time data exchange between production systems and enterprise resource planning platforms. Government initiatives such as the Gigabit Strategy provide funding support for fiber deployment in underserved regions, expanding the addressable market for optical components beyond major urban centers. The presence of leading telecommunications equipment manufacturers and system integrators further strengthens the domestic ecosystem for optical transceiver adoption.

United Kingdom Optical Transceivers Market Analysis

The United Kingdom was ranked second by holding 19.6% of the Europe optical transceiver market share in 2025 owing to the advanced telecommunications infrastructure and a thriving financial services sector that demands ultra low latency optical connectivity. The British optical transceiver market is distinguished by early adoption of high speed networking technologies and substantial investments in data center capacity to support cloud computing and artificial intelligence workloads. London status as a global financial center drives exceptional requirements for high frequency trading platforms and secure data transmission systems that rely on specialized optical transceivers with deterministic latency characteristics. The government Project Gigabit initiative allocates 5 billion pounds toward accelerating fiber deployment in hard to reach areas, stimulating procurement of optical components for last mile connectivity solutions. Furthermore, the financial services sector adherence to stringent regulatory requirements regarding data residency and transaction speed reinforces demand for high performance optical infrastructure within domestic borders.

France Optical Transceivers Market Analysis

France optical transceiver market market growth is likely to grow with the coordinated national infrastructure programs and strong domestic manufacturing capabilities that support optical component deployment across diverse sectors. This comprehensive rollout requires millions of optical transceivers for customer premises equipment, aggregation nodes, and core network upgrades throughout the country. The presence of major telecommunications operators and equipment manufacturers fosters a robust domestic ecosystem for optical technology development and deployment. The aerospace and defense sectors, which represent strategic industries for France, utilize specialized optical transceivers for secure communications and avionics systems, creating niche but high value market segments. Additionally, the government emphasis on digital sovereignty encourages procurement of optical components from European suppliers, benefiting domestic manufacturers and regional distribution channels.

Netherlands Optical Transceivers Market Analysis

The Netherlands optical transceiver market growth is likely to be driven by the strategic geographic position and advanced digital infrastructure to serve as a hub for European internet traffic and cloud services. As per the Netherlands Authority for Consumers and Markets, fiber to the home coverage exceeds 90% of households, among the highest rates in Europe, driving widespread adoption of optical network terminals and associated transceiver modules. Amsterdam functions as one of the continent primary internet exchange points, handling substantial volumes of international data traffic that necessitates robust optical transport infrastructure with advanced transceiver technologies. According to the Dutch Data Centre Association, the country hosts over 300 data center facilities, with major expansions underway to accommodate growing demand from hyperscale cloud providers and content delivery networks. The port of Rotterdam, Europe largest seaport, increasingly adopts fiber optic networks to support smart logistics and industrial automation applications, creating additional demand for optical transceivers in operational technology environments. Furthermore, the Netherlands strong commitment to sustainability encourages adoption of energy efficient optical components that align with national climate goals and corporate environmental responsibilities.

Spain Optical Transceivers Market Analysis

Spain optical transceiver market growth is prompting with an early dominance in fiber to the home deployments and growing investments in digital infrastructure to support tourism, telecommunications, and emerging technology sectors. The Spanish optical transceiver market benefits from one of Europe most extensive fiber optic networks, with coverage exceeding 90% of premises according to the National Markets and Competition Commission by creating sustained demand for optical network equipment and corresponding transceiver modules. This advanced infrastructure foundation enables service providers to offer gigabit speed broadband services that require high performance optical transceivers in customer premises equipment and aggregation systems. The tourism and hospitality sectors, which represent significant portions of the Spanish economy, increasingly adopt fiber connectivity to support digital guest experiences and operational efficiency, driving demand for optical components in commercial and public venues. As per the Spanish Ministry of Economic Affairs, investments in digital transformation initiatives exceeded 8 billion euros through the Recovery and Resilience Facility, with substantial allocations toward 5G deployment and smart city projects that further amplify optical transceiver demand. The presence of major telecommunications operators with aggressive network modernization strategies ensures continued procurement of advanced optical modules for backbone upgrades and access network expansions.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe optical transceiver market features intense rivalry among multinational semiconductor companies and specialized photonics manufacturers vying for leadership in high growth segments. Competition centers on technological differentiation with companies investing heavily in research to develop transceivers offering higher data rates, lower power consumption, and smaller form factors that meet evolving network architecture requirements. Price pressure remains significant in standardized product categories prompting manufacturers to optimize production efficiency through automation and economies of scale. Regulatory compliance regarding electromagnetic compatibility, safety certifications, and environmental standards creates additional competitive dimensions where companies with robust quality management systems gain advantages. The emergence of telecommunications and data center requirements has intensified competition as suppliers develop versatile optical modules capable of serving multiple application segments. Strategic alliances between transceiver manufacturers and system equipment providers have become increasingly common to secure long term supply agreements and share development risks for next generation technologies. Innovation in packaging technologies and thermal management serves as another battleground where companies seek to enable higher port densities without compromising reliability.

KEY MARKET PLAYERS

Some of the notable key players in the Europe optical transceiver market are

- Accelink Technologies

- Lumentum

- Innolight

- Sumitomo Electric Industries Ltd

- Coherent Corp

- Cisco Systems Inc

- Broadcom Inc

- Intel Corp

- Fujitsu Ltd

Top Players in the Market

- Broadcom Inc maintains a prominent position in the Europe optical transceiver market through its comprehensive portfolio of high speed connectivity solutions. The company contributes globally by pioneering silicon photonics technology that enables energy efficient data transmission for cloud infrastructure and telecommunications networks. Recent strategic actions include expanding its European engineering centers to accelerate development of 800 gigabit optical modules and establishing partnerships with regional cloud service providers to co design customized transceiver solutions. Broadcom commitment to innovation strengthens its European market position through advanced semiconductor manufacturing capabilities and localized technical support services. The company focus on power efficiency aligns with European sustainability mandates while delivering performance required for artificial intelligence workloads and hyperscale data center deployments across the continent.

- Intel Corporation leverages its silicon photonics expertise to serve the Europe optical transceiver market with high performance integrated optical solutions. The company global contribution centers on developing scalable manufacturing processes that reduce cost per bit for data center interconnects and telecommunications applications. Recent initiatives include investing in European research collaborations focused on co packaged optics and expanding production capacity for 400 gigabit transceivers at its facilities. Intel strategic partnerships with European telecommunications equipment manufacturers enable customized optical solutions that address regional network modernization requirements while advancing the company position in next generation connectivity markets. The organization commitment to open standards promotes interoperability across multi vendor European network environments.

- Lumentum Operations delivers advanced optical transceiver technologies to European telecommunications and data center customers through its specialized photonics portfolio. The company global impact stems from innovations in tunable lasers and coherent detection that enable long haul and metro network deployments. Recent actions to strengthen European presence include opening application engineering centers in key markets and launching new product lines optimized for 5G fronthaul and edge computing applications. Lumentum collaboration with European system integrators facilitates rapid deployment of optical solutions that support regional digital infrastructure expansion and cloud connectivity requirements. The company focus on reliability and performance ensures alignment with stringent European telecommunications standards and operational expectations.

Top Strategies Used by Key Market Participants

Key players in the Europe optical transceiver market employ strategic approaches to strengthen competitive positioning. Companies prioritize research and development investments to pioneer next generation silicon photonics and coherent optical technologies that deliver superior performance and energy efficiency. Strategic partnerships with telecommunications operators and cloud service providers enable co development of customized transceiver solutions aligned with specific network architecture requirements. Geographic expansion through localized engineering centers and technical support facilities improves customer responsiveness and reduces time to market for new products. Vertical integration strategies allow manufacturers to control critical component supply chains and ensure quality consistency across high volume production. Sustainability initiatives focusing on reduced power consumption and recyclable materials align with European environmental regulations and corporate procurement policies. Acquisition of specialized technology firms accelerates capability development in emerging areas such as co packaged optics and integrated photonics.

MARKET SEGMENTATION

This research report on the European optical transceiver market has been segmented and sub-segmented based on categories.

By Form Factor

- SFF and SFP

- SFP+ and SFP28

- QSFP, QSFP+, QSFP DD, QSFP28, QSFP56

- CFP, CFP2, CFP4, CFP8

- XFP

- CXP

By Data Rate

- Less than 10 Gbps

- 10 Gbps to 40 Gbps

- 41 Gbps to 100 Gbps

- More than 100 Gbps

By Fiber Type

- Single Mode Fiber (SMF)

- Multimode Fiber (MMF)

By Distance

- Less than 1 km

- 1 to 10 km

- 11 to 100 km

- More than 100 km

By Wavelength

- 850 nm band

- 1310 nm band

- 1550 nm band

- Other wavelengths

By Connector

- LC

- SC

- MPO

- RJ 45

By Protocol

- Ethernet

- Fiber Channels

- CWDM DWDM

- FTTX

- Other protocols

By Application

- Telecommunication

- Data Center

- Enterprise

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What is the current outlook of the Europe Optical Transceiver Market?

The Europe optical transceiver market is witnessing steady growth due to increasing demand for high speed data transmission, expansion of cloud computing services, and rising deployment of 5G and fiber optic networks across the region.

2.What factors are driving the growth of the Europe Optical Transceiver Market?

The market growth is driven by the rapid expansion of data centers, increasing internet traffic, rising adoption of cloud services, and growing investments in advanced telecommunications infrastructure.

3.What are optical transceivers and how are they used in communication networks?

Optical transceivers are devices that transmit and receive data through fiber optic cables by converting electrical signals into optical signals and are widely used in networking equipment such as switches, routers, and servers.

4.Which industries are the major end users of optical transceivers in Europe?

Major end users include telecommunications companies, cloud service providers, data center operators, enterprise networks, and government communication infrastructure.

5.Which countries are leading the Europe Optical Transceiver Market?

Germany, the United Kingdom, France, Italy, and the Netherlands are among the leading countries due to strong investments in digital infrastructure and data center development.

6.How is the growth of data centers influencing the Europe Optical Transceiver Market?

The rapid expansion of hyperscale and colocation data centers is increasing the demand for high speed optical transceivers to support large scale data transmission and network connectivity.

7.What types of optical transceivers are commonly used in Europe?

Common types include SFP, SFP Plus, QSFP, QSFP Plus, and QSFP28 transceivers that support different data transmission speeds and networking applications.

8.How is 5G deployment impacting the Europe Optical Transceiver Market?

The deployment of 5G networks is increasing the need for high capacity optical transceivers to support faster data transmission and improved network performance.

9.What are the key challenges in the Europe Optical Transceiver Market?

Challenges include high costs of advanced optical modules, compatibility issues with existing network equipment, and the need for continuous technological upgrades.

10.What role does cloud computing play in the Europe Optical Transceiver Market?

The increasing adoption of cloud computing services is driving demand for high speed networking infrastructure, which in turn boosts the need for advanced optical transceivers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com