Europe Tailgate Market Size, Share, Trends, and Growth Analysis Report, Segmented by Tailgate Type, Vehicle Type, Material, Sales Channel, and Country – Industry Forecast From 2026 to 2034

Europe Tailgate Market Report Summary

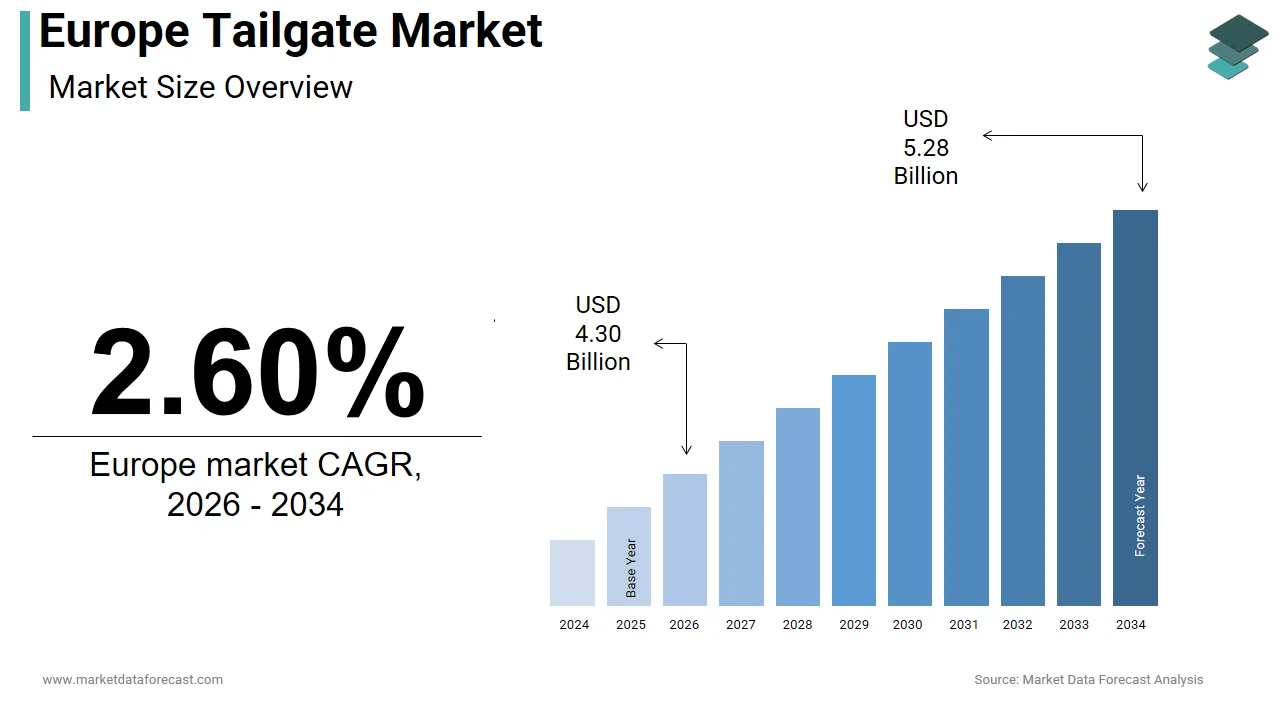

The Europe tailgate market was valued at USD 4.19 billion in 2025, is estimated to reach USD 4.30 billion in 2026, and is projected to reach USD 5.28 billion by 2034, growing at a CAGR of 2.60% from 2026 to 2034. Market growth is driven by steady automotive production, increasing demand for utility vehicles, and advancements in vehicle design and functionality. The growing integration of smart features such as power-operated and sensor-based tailgates, along with rising consumer preference for convenience and safety, is shaping market dynamics. However, the presence of cost-sensitive segments and mature automotive markets is moderating overall growth.

Key Market Trends

- Rising demand for utility vehicles across Europe.

- Increasing adoption of smart and power-operated tailgates.

- Focus on lightweight materials for fuel efficiency.

- Growth in automotive production and aftermarket sales.

- Integration of advanced safety and convenience features.

Segmental Insights

- Based on tailgate type, the manual tailgates segment dominated the Europe tailgate market by capturing 55.1% share in 2025, driven by cost-effectiveness and widespread adoption.

- Based on vehicle type, the utility vehicles segment led the market with 60.3% share in 2025, supported by increasing demand for SUVs and commercial vehicles.

- Based on material, the metal segment held the majority share in 2025, owing to its durability and structural strength.

- Based on sales channel, the OEM segment was the largest in 2025, driven by strong partnerships with automotive manufacturers.

Regional Insights

The Europe tailgate market shows stable growth across key automotive hubs.

- Germany led the market in 2025 with 28.2% share, driven by its strong automotive manufacturing base.

- France followed with 15.1% share, supported by established vehicle production and innovation.

- Spain plays a significant role due to its large-scale vehicle production capacity and export-oriented automotive industry.

Competitive Landscape

The Europe tailgate market is moderately competitive, with companies focusing on product innovation, lightweight materials, and integration of advanced features. Strategic collaborations with automotive OEMs and investments in smart tailgate systems are key competitive strategies.

Prominent companies operating in the Europe tailgate market include Magna International Inc., Faurecia, Robert Bosch GmbH, Brose Fahrzeugteile SE & Co. KG, Plastic Omnium, SEOYON E-HWA Automotive Slovakia, Rockland Manufacturing Company, Hi-Lex Corporation, Zhejiang Yuanchi Holding Group Co., Ltd., Gordon Auto Body Parts Co., Ltd., Huf Hülsbeck & Fürst GmbH & Co. KG, Woodbine Manufacturing Co. Inc., and Go Industries, Inc.

Europe Tailgate Market Size

The Europe tailgate market was valued at USD 4.19 billion in 2025. The regional market is projected to grow from USD 4.30 billion in 2026 to reach USD 5.28 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 2.60% from 2026 to 2034.

A tailgate is primarily a hinged board or door at the rear of a vehicle, such as a pickup truck or station wagon, that can be lowered or removed for loading and unloading. This market is critical to automotive body engineering, ensuring security, weather protection, and ergonomic access to cargo spaces. The market has evolved from simple manual latches to sophisticated power-operated and hands-free mechanisms driven by consumer demand for convenience and luxury features. As per data from the European Automobile Manufacturers’ Association (ACEA), the registrations of SUVs and crossovers, which heavily utilize advanced tailgate systems, accounted for approximately 51% of total passenger car sales in the European Union in 2023, surpassing the 50% threshold for the first time. This shift in vehicle preference directly influences the complexity and volume of tailgate components required. According to the International Organization of Motor Vehicle Manufacturers (OICA), Europe produced approximately 18.1 million motor vehicles in 2023, reflecting a robust recovery and a steady baseline demand for body closures. The regulatory landscape emphasizes pedestrian safety and crashworthiness, prompting innovations in lightweight materials such as aluminum and composite plastics to reduce overall vehicle mass. Furthermore, the integration of smart sensors for obstacle detection and automated opening sequences has become standard in premium segments. The presence of key tier one suppliers in Germany, France, and Italy fosters a competitive environment focused on technological refinement. Current trends indicate a move towards seamless integration with vehicle connectivity, allowing remote operation via smartphone applications. This technological convergence enhances user experience while addressing safety concerns related to accidental closures. The market is characterized by a balance between cost efficiency for mass market vehicles and high performance features for luxury segments, driving continuous innovation in actuation and locking mechanisms.

MARKET DRIVERS

Rising Popularity of SUVs and Crossovers Drives Demand for Advanced Closure Systems

The increasing consumer preference for sport utility vehicles and crossovers acts as a major accelerator for the Europe tailgate market. This is due to the inherent design requirements of these vehicle types. Unlike sedans, which utilize trunks, SUVs require large vertically opening tailgates that often incorporate complex lifting mechanisms and sealing systems. According to JATO Dynamics, SUVs and crossovers have secured the majority of new car sales in Europe, marking a historic shift where these vehicles now outsell traditional hatchbacks and estates. This structural change necessitates robust tailgate solutions capable of supporting heavier loads and larger surface areas. Manufacturers are responding by integrating power lift gates and hands-free access technologies as standard features even in mid-range models to enhance appeal. The ergonomic benefits of automated tailgates are particularly valued by families and elderly users who may struggle with manual operation. Furthermore, the versatility of SUV cargo spaces encourages the use of split tailgate designs, which allow for flexible loading options. These designs require precise engineering to ensure proper alignment and sealing against environmental elements. The trend towards larger vehicle dimensions also drives the need for stronger actuators and hinges that can withstand repeated use without failure. As the SUV segment continues to expand its dominance in the European automotive landscape, the demand for specialized tailgate systems will proportionally increase. This correlation ensures sustained growth for suppliers who can deliver reliable and innovative closure solutions tailored to the specific needs of modern utility vehicles.

Integration of Smart Connectivity and Automation Enhances User Convenience

Smart connectivity and automation technologies are rapidly transforming the Europe tailgate market. These innovations are enhancing vehicle functionality and user convenience. As a result, they are driving significant market growth. Modern consumers expect seamless interaction with their vehicles, leading to the adoption of hands-free tailgate systems activated by foot sensors or smartphone applications. According to the Deloitte Global Automotive Consumer Study, consumers in developing markets like China show high interest in connected features, whereas car buyers in Europe remain comparatively conservative, prioritizing basic functionality and price over advanced connectivity. This demand prompts manufacturers to equip vehicles with advanced sensors and control units that enable precise and safe tailgate operation. Hands-free systems are particularly beneficial in scenarios where users have their hands full, such as when carrying groceries or luggage. The technology relies on radar or capacitive sensors to detect movement and trigger the opening mechanism without physical contact. Additionally, the ability to control tailgate height and speed through vehicle settings allows for customization based on user preferences and garage clearance limits. The integration of these features also supports broader vehicle security systems by ensuring that the tailgate is properly locked and sealed before departure. As Internet of Things capabilities expand, tailgates are becoming part of the overall smart home ecosystem, allowing for remote monitoring and control. This technological evolution not only improves user experience but also differentiates brands in a competitive market. The continuous advancement in sensor accuracy and software reliability ensures that smart tailgates remain a key selling point for modern vehicles.

MARKET RESTRAINTS

High Production Costs of Advanced Mechanisms Restrain Market Expansion

The high production costs associated with advanced tailgate mechanisms hamper the growth of the Europe tailgate market. This is particularly true for entry-level and budget-friendly vehicles. Complex systems such as power lift gates and hands-free sensors require expensive components, including electric motors, control modules, and precision sensors. According to research, the integration of power tailgate systems adds significant component complexity and cost compared to simple manual strut assemblies, impacting the overall vehicle production budget. This cost increment poses a challenge for manufacturers aiming to keep vehicle prices competitive in a price-sensitive market segment. Economic pressures and inflation further exacerbate this issue as consumers become more cautious about discretionary spending on premium features. Consequently, many automakers reserve advanced tailgate technologies for higher trim levels or luxury models, limiting their widespread adoption. The complexity of these systems also increases maintenance and repair costs, which can deter potential buyers concerned about long-term ownership expenses. Supply chain disruptions for electronic components have further driven up prices and led to longer times, affecting production schedules. Small and medium-sized suppliers often struggle to absorb these costs, leading to consolidation in the supply chain. Until economies of scale reduce the cost of sensors and actuators, the penetration of advanced tailgate systems in mass market vehicles will remain limited. This financial barrier restricts market growth and forces manufacturers to carefully balance feature availability with affordability.

Stringent Safety Regulations Increase Compliance Complexity and Costs

Stringent safety regulations regarding pedestrian protection and crashworthiness impose serious constraints on the Europe tailgate market. This is achieved by increasing compliance complexity and development costs. Regulatory bodies such as the European New Car Assessment Program (Euro NCAP) mandate rigorous testing for occupant whiplash protection in rear impacts, while pedestrian safety protocols focus strictly on the vehicle's frontal structures. According to the European Commission, new vehicle types must comply with the updated General Safety Regulation, which mandates advanced technologies such as reversing detection systems and event data recorders to enhance road user safety. Meeting these standards requires extensive engineering efforts, including the use of energy-absorbing materials and reinforced structures, which add weight and cost to the vehicle. The need for anti-pinching sensors and obstacle detection systems further complicates the design process, requiring sophisticated software and hardware integration. Manufacturers must invest heavily in research and development to ensure that their tailgate systems meet all regulatory requirements without compromising functionality or aesthetics. The varying interpretation of regulations across different European countries can also create inconsistencies in compliance strategies. Additionally, the recall risk associated with faulty tailgate mechanisms poses a significant financial and reputational threat to manufacturers. Any failure to meet safety standards can result in costly recalls and legal liabilities. These regulatory burdens slow down the introduction of new technologies and increase the time to market for innovative tailgate solutions. Consequently, manufacturers must navigate a complex regulatory landscape that limits design flexibility and increases operational expenses.

MARKET OPPORTUNITIES

Development of Lightweight Materials Offers Growth Potential

The development and adoption of lightweight materials offer a significant opportunity for the European tailgate market. This addresses the dual demands of fuel efficiency and performance. Automakers are increasingly utilizing aluminum, carbon fiber reinforced plastics, and high-strength steel to reduce the overall weight of tailgates without compromising structural integrity. According to the European Aluminium Association, replacing traditional steel with aluminium for specific closures like tailgates can significantly reduce the weight of that individual component, contributing to better overall vehicle efficiency and reduced emissions. Lightweight tailgates also enhance the performance of power lift systems by reducing the load on actuators, thereby extending their lifespan and improving energy efficiency. The shift towards electric vehicles further amplifies the need for weight reduction to maximize battery range. Manufacturers are investing in advanced manufacturing techniques such as hydroforming and laser welding to produce complex lightweight structures cost-effectively. Collaborations between material suppliers and automotive OEMs are accelerating the innovation cycle, enabling the introduction of new composite materials with superior strength-to-weight ratios. These materials also offer design flexibility, allowing for more aerodynamic and aesthetically pleasing tailgate shapes. The environmental benefits of lightweighting align with sustainability goals, attracting eco-conscious consumers. By leveraging these material advancements, tailgate suppliers can offer value-added solutions that meet regulatory requirements and enhance vehicle performance. This technological progression opens new avenues for differentiation and growth in the competitive European automotive market.

Expansion of Aftermarket Customization and Retrofitting Services

The expansion of aftermarket customization and retrofitting services is creating new growth possibilities for the Europe tailgate market. This trend caters directly to owners seeking enhanced functionality and aesthetics. Many vehicle owners wish to upgrade their manual tailgates to power-operated systems or add hands-free capabilities after purchase. According to the European Association of Automotive Suppliers, the European automotive aftermarket represents a massive economic sector, with an increasing portion of revenue generated by advanced electronic upgrades and comfort-oriented features. Specialized companies are developing plug-and-play tailgate conversion kits that allow for easy installation without modifying the vehicle's original wiring harness. These products appeal to consumers who want the convenience of automated tailgates without the high cost of purchasing a new vehicle. The rise of e-commerce platforms has made these aftermarket solutions more accessible to a broader audience, facilitating direct-to-consumer sales. Additionally, the trend towards personalization drives demand for unique tailgate designs, including custom spoilers, integrated lighting, and distinctive badging. Workshops and service centers are expanding their offerings to include professional installation of these upgrades, ensuring quality and warranty coverage. The aging vehicle fleet in Europe also contributes to this opportunity as owners invest in maintaining and improving their existing cars. By tapping into the aftermarket segment, tailgate manufacturers and suppliers can diversify their revenue streams and reach customers beyond the original equipment channel. This growing sector offers sustainable growth potential driven by consumer desire for enhanced vehicle features.

MARKET CHALLENGES

Supply Chain Volatility for Electronic Components Disrupts Production

The volatility in the supply chain for critical electronic components, such as sensors, microcontrollers, and actuators, is a major limitation to the Europe tailgate market. Modern tailgate systems rely heavily on these electronics for automated operation and safety features, making them vulnerable to global supply disruptions. According to the European Automobile Manufacturers Association, while the most acute phase of the global chip crisis has passed, the industry remains sensitive to supply chain fluctuations that can still impact the production schedules of high-tech vehicle components. These disruptions lead to extended lead times and increased costs for tailgate manufacturers who struggle to secure consistent supplies. The concentration of semiconductor production in Asia exacerbates the risk, as geopolitical tensions and logistical bottlenecks can severely impact availability. Tailgate suppliers must maintain higher inventory levels to mitigate these risks, which ties up capital and increases storage costs. Additionally, the rapid technological evolution of electronic components requires continuous updates to design and sourcing strategies, adding complexity to supply chain management. The lack of local semiconductor manufacturing capacity in Europe means that the region remains dependent on imports, leaving it exposed to external shocks. Any delay in component delivery can halt entire production lines, affecting vehicle assembly schedules and customer deliveries. Ensuring a resilient and diversified supply chain is therefore a critical challenge for tailgate manufacturers. Addressing this vulnerability requires strategic partnerships and investment in local sourcing initiatives to stabilize production and meet market demand.

Technical Complexity of Integration with Vehicle Architecture

The technical complexity of integrating advanced tailgate systems with diverse vehicle architectures poses a significant challenge for manufacturers in the Europe tailgate market. Each vehicle model has unique structural dimensions, electrical systems, and software protocols requiring customized tailgate solutions. According to sources, the development cycle for a new tailgate system can take up to 3 years, involving extensive testing and validation to ensure compatibility and reliability. The integration of hands-free sensors and power actuators requires precise calibration to work seamlessly with the vehicle's central computer and other safety systems. Any mismatch in communication protocols can lead to malfunctioning features such as false triggering or failure to close. The increasing number of vehicle variants and platforms further complicates standardization efforts, forcing suppliers to develop multiple versions of similar components. This fragmentation increases development costs and reduces economies of scale. Additionally, the need for over-the-air software updates adds another layer of complexity as tailgate control units must be compatible with future software iterations. Manufacturers must invest in robust simulation and testing facilities to identify and resolve integration issues early in the design phase. The shortage of skilled engineers specializing in mechatronics and software integration further hinders the ability to manage this complexity. Failure to achieve seamless integration can result in poor user experience and increased warranty claims. Therefore, managing the technical intricacies of vehicle integration remains a persistent challenge for tailgate suppliers striving to deliver high-quality and reliable products.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Tailgate Type, Vehicle Type, Material, Sales Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered |

|

| Market Leaders Profiled | Magna International Inc., Faurecia, Robert Bosch GmbH, Brose Fahrzeugteile SE & Co. KG, Plastic Omnium, SEOYON E-HWA Automotive Slovakia, Rockland Manufacturing Company, Hi Lex Corporation, Zhejiang Yuanchi Holding Group Co., Ltd., Gordon Auto Body Parts Co., Ltd., Huf Hülsbeck & Fürst GmbH & Co. KG, Woodbine Manufacturing Co. Inc., Go Industries, Inc., and Others. |

SEGMENTAL ANALYSIS

By Tailgate Type Insights

In 2025, the manual tailgates segment dominated the Europe tailgate market and accounted for a 55.1% share. This dominance of the segment is driven by its cost efficiency and mechanical reliability, which are critical factors for mass market vehicle production. Unlike power-operated systems, manual tailgates do not require expensive electric motors, sensors, or control units, significantly reducing the bill of materials. According to research, the cost difference between manual and power liftgate systems is a primary consideration for volume manufacturers, as the electronic and hydraulic components required for automation significantly increase the per-unit production expense. This cost advantage allows automakers to keep entry-level vehicles affordable while maintaining profitability. Furthermore, manual tailgates are less prone to electronic failures and require minimal maintenance, enhancing their appeal to budget-conscious consumers. The simplicity of the mechanism ensures long-term durability even under harsh weather conditions, which is a key consideration in various European climates. Many compact cars and lower trim levels of SUVs continue to rely on manual tailgates as standard equipment. The widespread availability of replacement parts and ease of repair further support their dominance. As economic pressures influence consumer choices, the demand for cost-effective solutions remains strong. Consequently, manual tailgates continue to be the preferred choice for a significant portion of the European automotive fleet, ensuring their leading position in the market. The domination of the manual segment is further reinforced by its standardization across entry-level and compact vehicle segments, which constitute a large volume of European car sales. Manufacturers often reserve advanced features like power tailgates for higher trim levels or premium models to differentiate product offerings. According to data from JATO Dynamics, compact and subcompact cars accounted for over 30 percent of new car registrations in Europe in 2023, with the majority featuring manual tailgates. This segmentation strategy allows brands to offer a base model at a competitive price point while upselling convenience features as optional extras. The manual tailgate serves as a functional and reliable solution that meets the basic needs of most drivers without adding unnecessary complexity. In urban environments where parking spaces are tight and loading heights are low, the physical effort required to operate a manual tailgate is minimal, making it a practical choice. Additionally, the lighter weight of manual systems contributes to overall vehicle fuel efficiency, aligning with emission reduction goals. The established supply chain for manual components ensures consistent quality and timely delivery. As long as there is a robust market for affordable transportation, manual tailgates will remain a staple in the European automotive landscape. Their ubiquity and proven track record solidify their status as the leading segment.

The power-operated tailgate segment is likely to experience the fastest CAGR of 7.8% from 2026 to 2034 due to increasing consumer demand for convenience and accessibility features, particularly among aging populations and families. Power tailgates allow users to open and close the rear door with the push of a button or via hands-free sensors, eliminating the need for physical exertion. According to consumer preference studies, a significant number of SUV buyers in premium segments prioritize automated liftgates for their convenience, though this demand varies across different European national markets based on vehicle size and price point. This preference is especially pronounced in premium and mid-range segments where comfort and luxury are key selling points. The integration of hands-free technology, which activates the tailgate with a foot gesture, further enhances convenience for users carrying groceries or luggage. Automakers are responding by making power tailgates standard equipment in more models to remain competitive. The ability to program opening height settings also adds to the user-friendly nature of these systems. As the population ages, the demand for accessible vehicle features will continue to rise, driving growth in this segment. The perceived value addition of power tailgates justifies the higher cost for many consumers, ensuring sustained adoption rates. The accelerated growth of the power-operated segment is also fueled by its seamless integration with smart vehicle ecosystems and connectivity features. Modern power tailgates are no longer standalone mechanisms but are integrated into the vehicle's central computer, allowing for remote operation via smartphone applications. According to the European Automobile Manufacturers Association, the total number of vehicles on European roads continues to grow, with an increasing percentage of the fleet featuring integrated connectivity that enables remote and intelligent tailgate operations. Users can open or close their tailgates remotely, enabling convenient loading and unloading without being near the vehicle. This connectivity also supports enhanced security features such as automatic locking and anti-pinch protection, which prevent accidents and theft. The integration with voice assistants and home automation systems further expands the utility of power tailgates. For instance, users can command their vehicle to open the tailgate using voice commands through smart speakers. These advanced capabilities differentiate modern vehicles and appeal to tech-savvy consumers who value innovation. As automotive software becomes more sophisticated, the functionality of power tailgates will continue to evolve, offering new features and improvements. This technological synergy ensures that power-operated tailgates remain at the forefront of market growth.

By Vehicle Type Insights

The utility vehicles segment led the Europe tailgate market and attributed to 60.3% share in 2025. This leading position of the segment is attributed to the overwhelming popularity of SUVs in the European automotive market. The design of these vehicles inherently requires a large rear tailgate for cargo access, making them the primary consumers of tailgate systems. The trend towards larger and more versatile vehicles has led to increased production volumes, thereby driving demand for both manual and power-operated tailgates. Manufacturers are expanding their SUV portfolios to cater to diverse customer segments from compact urban crossovers to full-size family haulers. Each of these variants requires specialized tailgate solutions tailored to their specific dimensions and usage patterns. The versatility of SUVs for both urban commuting and outdoor activities further boosts their appeal. As consumers continue to prioritize space and flexibility, utility vehicles remain the top choice for European buyers. This sustained demand ensures that the utility vehicle segment remains the largest consumer of tailgate technologies in the region. The leadership of the utility vehicle segment is further reinforced by the requirement for robust and versatile closure systems that can handle heavy loads and frequent use. SUV tailgates are often larger and heavier than those on passenger cars, necessitating stronger actuators and hinges. The need for durability drives innovation in material science and mechanical design within the tailgate market. Manufacturers are developing high-strength steel and aluminum components to ensure longevity and reliability. The integration of split tailgate designs, which allow for independent opening of upper and lower sections, adds complexity but enhances functionality for loading heavy items. These specialized requirements create a distinct market niche for high-performance tailgate systems. The premium nature of many SUVs also encourages the adoption of advanced features such as power operation and hands-free access. As utility vehicles continue to evolve with new features and capabilities, the demand for sophisticated tailgate solutions will remain strong. This technical necessity solidifies the position of utility vehicles as the leading segment in the tailgate market.

The commercial vehicle segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 6.5% during the forecast period, owing to the booming e-commerce sector, which has drastically increased the demand for last-mile delivery services. These vehicles require efficient and durable tailgates to facilitate quick loading and unloading of packages. The shift towards electric LCVs also influences tailgate design as manufacturers seek lightweight solutions to maximize battery range. Automated tailgates are increasingly being adopted in commercial fleets to improve driver efficiency and reduce physical strain. The ability to operate tailgates remotely or via foot sensors allows drivers to keep their hands free for handling parcels. This operational efficiency is crucial for meeting tight delivery schedules in urban environments. As logistics companies expand their fleets to meet growing demand, the market for commercial vehicle tailgates will continue to grow. The focus on productivity and ergonomics ensures that this segment experiences robust expansion in the coming years. The quick surge of the commercial vehicle segment is also fueled by regulatory pressures promoting fleet electrification and operational efficiency. The European Union has set ambitious targets for reducing carbon emissions from transport, prompting many companies to transition to electric LCVs. Electric LCVs often feature unique body structures and weight distributions requiring specialized tailgate designs. Manufacturers are developing lightweight and energy-efficient tailgate systems to complement the sustainability goals of electric fleets. Additionally, regulations regarding worker safety and ergonomics are encouraging the adoption of automated tailgates to reduce the risk of injury during loading operations. Government incentives for green logistics further support the uptake of modern commercial vehicles equipped with advanced features. The need for reliable and low-maintenance tailgates is paramount for commercial operators who rely on their vehicles for daily business. As the commercial sector undergoes a fundamental transformation towards sustainability and efficiency, the demand for innovative tailgate solutions will continue to rise. This regulatory and operational shift ensures that the commercial vehicle segment remains the fastest-growing area in the market.

By Material Insights

The metal segment held the majority share of the Europe tailgate market in 2025. This supremacy of the segment is credited to its superior structural integrity and durability. Steel and aluminum are the primary materials used in tailgate construction due to their ability to withstand impact and provide robust protection for cargo. Metal tailgates offer excellent resistance to deformation and damage, which is essential for maintaining vehicle safety and aesthetics. The material also provides a solid foundation for mounting hardware such as hinges, locks, and wipers. Aluminum is increasingly being used in premium vehicles to reduce weight while maintaining strength, contributing to improved fuel efficiency. The established manufacturing processes for metal tailgates, including stamping and welding, ensure high production efficiency and consistency. The recyclability of metal aligns with sustainability goals, as end-of-life vehicles are processed for material recovery. Despite the emergence of alternative materials, metal remains the benchmark for reliability and performance in automotive closures. Its widespread availability and competitive pricing further cement its dominance. As long as structural strength remains a priority, metal will continue to be the material of choice for the majority of tailgates in the European market. The leading position of the metal segment is further reinforced by its cost-effectiveness and well-established supply chains. Metal components are generally cheaper to produce than advanced composites or plastics, especially at high volumes. The extensive network of suppliers and processors for automotive metals ensures timely delivery and quality control. This reliability is crucial for automotive production lines that operate on just-in-time principles. Metal tailgates can be easily repaired and painted to match the vehicle body color seamlessly, which is important for aesthetic consistency. The familiarity of repair shops with metal work also reduces maintenance costs for consumers. While lightweight alternatives are gaining traction, the economic advantages of metal make it difficult to replace in mass market vehicles. Manufacturers continue to optimize metal designs through advanced high-strength steels, which offer better performance without significant cost increases. This balance of cost performance and availability ensures that metal remains the leading material in the tailgate market. The ongoing innovation in metal alloys further extends its relevance in modern automotive design.

The plastic segment is expected to exhibit a noteworthy CAGR of 5.2% during the forecast period. This swift growth of the segment is mainly supported by the automotive industry's relentless pursuit of weight reduction to improve fuel efficiency and reduce emissions. Plastics such as polypropylene and ABS are significantly lighter than metal, offering substantial weight savings without compromising structural integrity. The weight reduction is particularly beneficial for electric vehicles, where every kilogram saved contributes to an extended battery range. Plastic tailgates also offer greater design flexibility, allowing for complex shapes and integrated features such as spoilers and lighting elements. Injection molding techniques enable the production of intricate designs that are difficult or expensive to achieve with metal. The ability to mold color directly into the plastic eliminates the need for painting, reducing production costs and environmental impact. As automakers strive to meet stringent emission standards, the adoption of lightweight plastic tailgates is accelerating. This material innovation supports the broader industry goal of sustainable mobility, ensuring rapid growth for the plastic segment. The accelerated growth of the plastic segment is also fueled by its inherent corrosion resistance and lower manufacturing costs. Unlike metal, plastics do not rust, making them ideal for tailgates, which are exposed to rain, snow, and road salt. The production process for plastic tailgates is also more efficient as it involves fewer steps than metal fabrication. Injection molding allows for high-volume production with minimal waste and energy consumption. This efficiency translates to lower unit costs, making plastic an attractive option for cost-sensitive segments. Additionally, plastics can be easily recycled, supporting circular economy initiatives in the automotive industry. The development of bio-based and recycled plastics further enhances the sustainability profile of this material. Automakers are increasingly incorporating recycled content into tailgate production to meet environmental targets. The combination of durability, cost efficiency, and eco-friendliness makes plastic a compelling alternative to metal. As technology advances, the performance of engineering plastics continues to improve, bridging the gap with traditional materials. This trajectory ensures that plastic will experience the fastest growth in the tailgate market.

By Sales Channel Insights

The Original Equipment Manufacturers (OEMs) segment was the largest segment in the Europe tailgate market and occupied a substantial share in 2025 because of the direct integration of tailgate systems into vehicle production lines during the manufacturing process. Every new vehicle produced requires a tailgate, making OEMs the primary channel for distribution. The massive volume ensures a steady and predictable demand for tailgate suppliers who partner directly with automakers. OEM contracts are typically long-term, providing stability and economies of scale for manufacturers. The close collaboration between suppliers and OEMs allows for customized designs that meet specific vehicle requirements and brand standards. Quality control and testing are rigorous, ensuring that only high-performance products reach the market. The barrier to entry for new suppliers is high due to strict certification processes, fostering a consolidated market structure. As vehicle production volumes remain robust, the OEM channel will continue to dominate. The inability of the aftermarket to match this scale ensures that OEMs remain the primary revenue source for the tailgate industry. The leadership of the OEM segment is further reinforced by strict quality standards and the need for brand consistency. Automakers require tailgates that seamlessly integrate with the vehicle design and function flawlessly throughout its lifecycle. The level of assurance is critical for maintaining brand reputation and customer satisfaction. OEMs invest heavily in research and development to innovate tailgate features such as power operation and smart connectivity. These innovations are first introduced through the OEM channel before becoming available in the aftermarket. The exclusivity of proprietary technologies and designs further strengthens the OEM position. Consumers trust original parts for their fit and finish, preferring them over generic alternatives. The warranty coverage provided by OEMs also adds value, encouraging buyers to stick with original equipment. As vehicles become more complex, the importance of precise engineering and integration grows. This reliance on specialized knowledge and quality assurance ensures that OEMs maintain their dominant share in the tailgate market.

The aftermarket segment is predicted to witness the highest CAGR of 4.5% between 2026 and 2034. This rapid growth of the segment is primarily fuelled by the aging vehicle fleet in Europe and the increasing demand for retrofitting solutions. Owners are increasingly opting to replace damaged or malfunctioning tailgates rather than purchasing new vehicles. The rise of e-commerce has made aftermarket parts more accessible and affordable, allowing consumers to easily find replacements. Specialized kits for upgrading manual tailgates to power-operated systems are also gaining popularity among enthusiasts. These retrofitting solutions offer a cost-effective way to enhance vehicle convenience and value. The availability of certified replacement parts from third-party suppliers ensures quality and reliability. As consumers seek to extend the life of their vehicles, the aftermarket channel will continue to expand. The focus on customization and upgrades further fuels growth in this segment. The accelerated growth of the aftermarket segment is also fueled by the expansion of independent repair shops and online retailers. These channels provide competitive pricing and faster service compared to authorized dealerships. Online platforms allow customers to compare prices and read reviews, making it easier to choose the right product. The convenience of home delivery and easy return policies enhances the customer experience. Independent workshops are also adopting advanced diagnostic tools and training, enabling them to handle complex tailgate repairs and installations. The availability of instructional videos and online guides empowers DIY enthusiasts to perform their own replacements. This democratization of access to parts and information drives aftermarket sales. As digital transformation continues to reshape retail, the aftermarket channel will benefit from increased visibility and reach. The combination of affordability, convenience, and variety ensures that the aftermarket remains the fastest-growing segment in the tailgate market.

COUNTRY LEVEL ANALYSIS

Germany Tailgate Market Analysis

Germany was the top performer in the Europe tailgate market and accounted for a 28.2% in 2025. This dominance of the German market is driven by its robust automotive manufacturing industry. The country is home to major original equipment manufacturers such as Volkswagen, BMW, and Mercedes-Benz, which produce millions of vehicles annually. The presence of leading tier one suppliers such as Brose and Hella further strengthens the market ecosystem. German automakers are at the forefront of integrating advanced tailgate technologies, including power liftgates and hands-free sensors. The strong emphasis on engineering precision and quality ensures that German-made tailgates meet high global standards. The country's focus on electric vehicle production also drives innovation in lightweight tailgate materials. Government incentives for automotive research and development support continuous improvement in closure systems. The extensive supplier network in Germany facilitates efficient production and distribution. The domestic demand for premium vehicles with advanced features further boosts the market. Germany's leadership in automotive technology and manufacturing ensures its dominant role in the regional tailgate market.

France Tailgate Market Analysis

France followed closely behind in the Europe tailgate market and occupied a 15.1% share in 2025. This growth of the French market is supported by a strong domestic automotive industry. The country hosts major manufacturers such as Stellantis, which produces a wide range of passenger and commercial vehicles. The presence of specialized suppliers and research centers fosters innovation in tailgate design and materials. French automakers are increasingly focusing on electric and hybrid vehicles, which require lightweight and efficient tailgate solutions. The government supports the sector through initiatives promoting sustainable mobility and industrial modernization. The demand for utility vehicles and vans for logistics services also contributes to market growth. France's strategic location within Europe facilitates the easy distribution of components to neighboring countries. The country's expertise in design and aesthetics influences tailgate styling and integration. The ongoing transition towards electrification drives the adoption of advanced tailgate technologies. France's strong industrial base and commitment to innovation ensure its continued relevance in the European tailgate market.

Spain Tailgate Market Analysis

Spain plays a major role in the Europe tailgate market due to its large vehicle production capacity. The country is one of the largest automobile producers in Europe, with major plants operated by Stellantis, Volkswagen, and Ford. The Spanish automotive industry is increasingly focusing on electric vehicle production, with several manufacturers announcing plans to convert existing plants. This transition boosts the demand for modern tailgate solutions that align with new vehicle architectures. Spain has a growing network of tier one and tier two suppliers specializing in body components, including tailgates. The government supports the sector through strategic projects aimed at modernizing the automotive industry. The availability of skilled labor and competitive production costs make Spain an attractive location for manufacturing. The country's strategic location provides easy access to both European and North African markets. Spanish suppliers are investing in automation and digital technologies to enhance productivity. The focus on exporting vehicles and components further strengthens Spain's position in the regional market.

United Kingdom Tailgate Market Analysis

The United Kingdom maintains a strong position in the Europe tailgate market despite the challenges posed by Brexit. The country has a prestigious automotive heritage with luxury brands like Jaguar Land Rover and Bentley demanding high-performance tailgate systems. The UK government has banned the sale of new petrol and diesel cars from 2030, accelerating the shift towards electric vehicles and associated tailgate technologies. This policy drives demand for lightweight and automated tailgate units that are essential for new energy vehicles. The UK is also a center for automotive research and development, with universities and tech firms collaborating on advanced materials. The presence of specialized engineering firms supports the development of innovative tailgate concepts. However, supply chain disruptions and trade barriers have introduced complexities for manufacturers sourcing components from the EU. Despite these challenges, the UK remains a key market for premium and specialized tailgate solutions. The focus on high-value segments allows UK manufacturers to compete effectively on quality and technology.

Italy Tailgate Market Analysis

Italy is anticipated to grow significantly in the Europe tailgate market from 2026 to 2034, owing to its strong presence in both passenger car and commercial vehicle manufacturing. The country is home to Fiat Chrysler Automobiles, now part of Stellantis, which produces a wide range of vehicles requiring reliable tailgate systems. Italy is also renowned for its luxury and sports car manufacturers, which require high-performance tailgate solutions for superior aesthetics and functionality. These niche segments drive innovation in tailgate technology with a focus on design and integration. The Italian government supports the automotive industry through incentives for electric vehicle purchases and infrastructure development. This support encourages the adoption of advanced tailgate systems in new models. Italy has a dense network of specialized suppliers and engineering firms that contribute to the global tailgate supply chain. The country's expertise in design and engineering allows it to produce high-value-added components. The transition towards electrification is gaining momentum with Italian manufacturers launching new electric models. The focus on quality and performance ensures that Italy remains a relevant and influential player in the European tailgate market.

COMPETITIVE LANDSCAPE

The competition in the Europe tailgate market is intense, characterized by the presence of established global suppliers and specialized regional manufacturers. Major players compete on technological innovation, product quality, and ability to meet stringent environmental regulations. The shift towards electric vehicles and automated features has intensified rivalry as companies race to develop lightweight and smart tailgate systems. Price pressure from automakers remains a challenge, forcing suppliers to optimize costs through efficient manufacturing and economies of scale. Differentiation is achieved through superior engineering expertise and integrated software solutions that enhance user experience. Strategic alliances with tech companies are common as firms seek to incorporate artificial intelligence and connectivity features. The market also sees new entrants focusing on niche segments such as retrofitting and aftermarket solutions. Regulatory compliance acts as a barrier to entry, ensuring that only capable players sustain operations. Continuous investment in research and development is essential to stay ahead in this dynamic landscape where technological superiority dictates market leadership and long-term success for all participating entities in the European automotive supply chain.

KEY MARKET PLAYERS

The leading companies operating in the Europe tailgate market include:

- Magna International Inc.

- Faurecia

- Robert Bosch GmbH

- Brose Fahrzeugteile SE & Co. KG

- Plastic Omnium

- SEOYON E-HWA Automotive Slovakia

- Rockland Manufacturing Company

- Hi Lex Corporation

- Magna International Inc.

- Zhejiang Yuanchi Holding Group Co., Ltd.

- Gordon Auto Body Parts Co., Ltd.

- Huf Hülsbeck & Fürst GmbH & Co. KG

- Woodbine Manufacturing Co., Inc.

- Go Industries, Inc.

TOP PLAYERS IN THE MARKET

- Brose Fahrzeugteile is a leading global supplier of mechatronic systems with a strong presence in the Europe tailgate market. The company specializes in developing innovative power liftgate systems and hands-free access solutions that enhance vehicle convenience. Brose contributes to the global market by supplying advanced closure systems to major automotive manufacturers worldwide. Recent actions include expanding its production capabilities for electric drive systems tailored for heavy-duty tailgates. The company also invests heavily in research and development to integrate smart sensors and connectivity features. These initiatives strengthen its market position by offering comprehensive and reliable tailgate solutions. Brose focuses on lightweight design and energy efficiency, aligning with industry trends towards sustainability. Its commitment to quality and innovation ensures continued leadership in the competitive European automotive supply chain.

- Magna International is a diversified mobility supplier with significant involvement in the Europe tailgate market through its body exterior and closure systems division. The company provides complete tailgate modules, including structures, mechanisms, and electronic controls. Magna contributes globally by leveraging its integrated manufacturing capabilities to deliver cost-effective and high-quality solutions. Recent actions include the development of lightweight composite tailgates that reduce vehicle weight and improve fuel efficiency. The company also enhances its digital engineering tools to accelerate product development cycles. These efforts strengthen its market position by offering customized and innovative tailgate systems. Magna focuses on sustainability by using recycled materials and optimizing production processes. Its global footprint and technical expertise enable it to meet the diverse needs of European automakers while maintaining a competitive edge in technology and service.

- Hi Lex Corporation is a prominent player in the Europe tailgate market, known for its expertise in automotive body hardware and closure systems. The company supplies a wide range of tailgate components, including hinges, latches, and power liftgate actuators. Hi Lex contributes to the global market by providing reliable and durable solutions to various automotive brands. Recent actions include the expansion of its European manufacturing facilities to increase production capacity and reduce lead times. The company also invests in advanced testing laboratories to ensure product quality and performance. These initiatives strengthen its market position by delivering consistent and high-standard tailgate systems. Hi Lex focuses on continuous improvement and customer collaboration to develop tailored solutions. Its strategic partnerships with OEMs enable it to stay ahead of market trends and technological advancements in the European automotive sector.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe tailgate market primarily focus on product innovation and strategic partnerships to maintain their competitive edge. Companies invest heavily in research and development to create lightweight and energy-efficient tailgate systems that support vehicle electrification. Collaborations with technology firms enable the integration of smart sensors and connectivity features into tailgate mechanisms. Manufacturers also expand their production facilities in Europe to reduce supply chain risks and meet local demand efficiently. Sustainability is a core strategy with firms adopting green manufacturing processes and using recycled materials. Additionally, companies pursue mergers and acquisitions to acquire specialized skills and technologies in mechatronics. These strategies help participants offer comprehensive solutions that comply with strict European regulations while enhancing vehicle convenience and safety for consumers across the region.

MARKET SEGMENTATION

This research report on the Europe tailgate market has been segmented and sub-segmented into the following categories.

By Tailgate Type

- Hydraulic Operated

- Power Operated

- Manual

By Vehicle Type

-

- Passenger Vehicle

- Hatchback

- Sedan

- Utility Vehicle

- Commercial Vehicle

- LCV

- HCV

- Bus

- Passenger Vehicle

By Material

- Metal

- Plastic

- Others

By Sales Channel

- OMEs

- Aftermarket

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe tailgate market?

The Europe tailgate market covers rear vehicle access systems used in passenger and commercial vehicles. It includes manual and powered tailgates designed for safety, convenience, and lightweight performance.

How does the Europe tailgate market function?

The Europe tailgate market functions through OEM supply chains, where automakers source rear closure systems, hinges, actuators, sensors, and control modules for vehicle assembly.

What drives growth in the Europe tailgate market?

The Europe tailgate market grows because automakers want lighter vehicles, better safety, and more convenience features such as powered and hands-free opening systems.

Which countries lead the Europe tailgate market?

The Europe tailgate market is led by Germany, France, the UK, and Italy, where major automakers and component suppliers support strong demand for advanced tailgate systems.

What types define the Europe tailgate market?

The Europe tailgate market includes manual tailgates, powered tailgates, smart tailgates, and liftgate systems used across different vehicle segments and trim levels.

What vehicle segments shape the Europe tailgate market?

The Europe tailgate market is shaped by passenger cars, SUVs, crossovers, and light commercial vehicles, where rear access convenience is a key consumer feature.

How does regulation influence the Europe tailgate market?

The Europe tailgate market is influenced by vehicle safety standards, crash regulations, and lightweighting goals that encourage stronger and more efficient tailgate designs.

What trends affect the Europe tailgate market?

The Europe tailgate market is influenced by power-opening systems, sensor-based automation, premium comfort features, and demand for lighter body components.

What challenges face the Europe tailgate market?

The Europe tailgate market faces cost pressure, integration complexity, and the need to balance weight reduction with durability, safety, and noise performance.

How does electrification impact the Europe tailgate market?

The Europe tailgate market benefits from electrification because EVs and premium models often include powered rear access systems as standard or optional features.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com