Europe Tissue Engineering Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, End-User, and Country – Industry Forecast From 2026 to 2034

Europe Tissue Engineering Market Report Summary

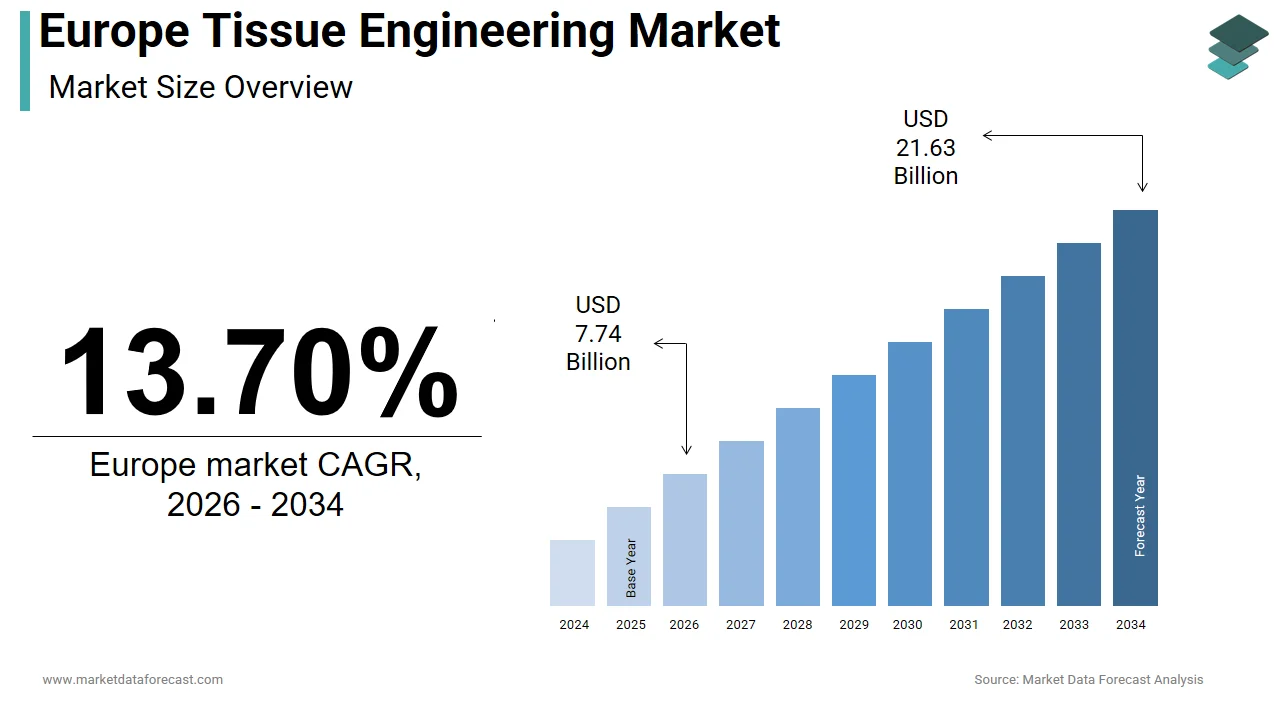

The Europe tissue engineering market was valued at USD 8.61 billion in 2025, is estimated to reach USD 7.74 billion in 2026, and is projected to reach USD 21.63 billion by 2034, growing at a CAGR of 13.70% from 2026 to 2034. Market growth is driven by increasing demand for regenerative medicine, rising prevalence of chronic diseases, and advancements in biomaterials and stem cell technologies. Tissue engineering solutions are widely used for repairing or replacing damaged tissues, particularly in orthopedic, wound care, and reconstructive applications. Growing investments in biotechnology, increasing clinical research, and expanding applications of 3D bioprinting are further accelerating market growth across Europe.

Key Market Trends

- Increasing adoption of regenerative medicine and tissue engineering solutions.

- Advancements in biomaterials, stem cell research, and 3D bioprinting.

- Rising demand for orthopedic and wound healing applications.

- Growing investments in biotechnology and life sciences research.

- Expansion of personalized medicine and advanced therapeutic solutions.

Segmental Insights

- Based on type, the scaffolds segment dominated the Europe tissue engineering market by capturing 58.9% share in 2025, driven by their critical role in supporting tissue regeneration.

- Based on application, the orthopedic segment led the market with 42.8% share in 2025, supported by increasing cases of bone injuries and degenerative disorders.

- Based on end user, the hospitals and ambulatory surgical centers (ASCs) segment held a substantial share in 2025, driven by high adoption of advanced regenerative therapies.

Regional Insights

The Europe tissue engineering market is witnessing strong growth across major countries due to innovation in biomedical research and healthcare advancements.

- Germany led the regional market in 2025 with 24.7% share, supported by advanced research infrastructure and strong manufacturing capabilities.

- The United Kingdom followed with 18.5% share in 2025, driven by robust research institutions and increasing healthcare innovation.

- France holds a significant position due to strong government initiatives, centralized healthcare systems, and growing focus on biotechnology.

Competitive Landscape

The Europe tissue engineering market is competitive, with the presence of biotechnology firms, medical device companies, and regenerative medicine specialists. Market players are focusing on product innovation, expanding clinical applications, and strengthening research collaborations. Investments in advanced biomaterials and regenerative therapies are shaping competitive dynamics across the region.

Prominent companies operating in the Europe tissue engineering market include AlloSource, Integra LifeSciences Corporation, Zimmer Biomet Holdings Inc., MIMEDX Group, Inc., Organogenesis Holdings Inc., Medtronic plc, Smith+Nephew, Tissue Regenix, VIVEX Biologics, Inc., Stryker, and BioTissue.

Europe Tissue Engineering Market Size

The size of the Europe tissue engineering market was worth USD 8.61 billion in 2025. The regional market is anticipated to grow at a CAGR of 13.70% from 2026 to 2034 and be worth USD 21.63 billion by 2034 from USD 7.74 billion in 2026.

Tissue engineering is a multidisciplinary field that combines biology, engineering, and materials science to create biological substitutes that can restore, maintain, or improve the function of damaged tissues or entire organs. This domain extends beyond simple repair mechanisms to encompass the regeneration of complex organs and structures using scaffolds, cells, and bioactive molecules. The European landscape is uniquely shaped by a robust regulatory framework under the European Medicines Agency, which classifies many of these products as Advanced Therapy Medicinal Products. Demographic shifts play a pivotal role in defining the current scenario, as the region faces an aging population that significantly increases the prevalence of degenerative conditions. According to Eurostat, individuals aged 65 and older constituted 21.6% of the total European Union population in 2024, creating an unprecedented demand for regenerative solutions to address age-related tissue deterioration. Furthermore, the burden of chronic diseases remains substantial, with the World Health Organization indicating that non-communicable diseases account for around 90% of all deaths in the European region. This epidemiological reality drives the necessity for innovative therapeutic approaches that traditional pharmacology cannot fully address. The integration of nanotechnology and 3D bioprinting within European research institutions further accelerates the translation of laboratory discoveries into clinical applications, positioning the continent as a global hub for regenerative medicine innovation.

MARKET DRIVERS

Rising incidence of osteoarthritis and cardiovascular failure drives urgent demand for regenerative alternatives.

The escalating incidence of chronic degenerative disorders works as a strong booster for the expansion of the Europe tissue engineering market. Conditions such as osteoarthritis, cardiovascular diseases, and chronic wounds impose a massive burden on healthcare systems and patients alike, creating an urgent need for regenerative therapies that offer long-term restoration rather than temporary symptom management. Osteoarthritis alone affects a significant portion of the elderly demographic. The European Alliance of Associations for Rheumatology highlights the significant and growing burden of osteoarthritis across the continent, identifying it as a leading cause of disability that necessitates advanced therapeutic interventions. This widespread prevalence drives the demand for cartilage repair technologies and bone graft substitutes that can delay or eliminate the need for joint replacement surgeries. Similarly, the European Society of Cardiology reports that ischemic heart disease affects a vast number of patients annually, driving the demand for advanced vascular grafts and cardiac patches designed to restore and repair damaged heart tissue. The limitations of donor organ availability further exacerbate this demand, as waiting lists for transplants continue to grow while donor rates stagnate. Tissue-engineered constructs provide a viable alternative by utilizing autologous cells to create functional tissues that integrate seamlessly with the host body. This shift towards regenerative medicine is supported by increasing healthcare expenditure on chronic disease management, compelling stakeholders to invest in technologies that reduce long term care costs and improve patient quality of life through biological restoration.

Breakthroughs in biodegradable polymers and responsive materials accelerate clinical translation.

Rapid progress in biomaterial science and the refinement of regenerative technologies constitute a major driver fuelling the Europe tissue engineering market expansion. The development of novel scaffolds composed of biodegradable polymers, ceramics, and composite materials has revolutionized the ability to mimic the extracellular matrix and support cell proliferation and differentiation. European research consortia have been at the forefront of designing smart biomaterials that respond to physiological cues and release growth factors in a controlled manner to enhance tissue regeneration. The European Commission has allocated substantial funding through its Horizon Europe program to support interdisciplinary projects that bridge material science with clinical application, fostering an environment of continuous innovation. Strategic initiatives within the European Union have led to a marked increase in funding for advanced biomaterials research, reflecting a clear policy priority to maintain a competitive edge in medical innovation. Furthermore, the integration of 3D bioprinting technologies allows for the precise deposition of cells and biomaterials to create complex tissue architectures that were previously impossible to engineer. This capability is particularly crucial for developing patient-specific implants that match individual anatomical requirements, thereby reducing rejection risks and improving surgical outcomes. The collaboration between academic institutions and biotechnology firms in countries like Germany, France, and the United Kingdom accelerates the commercialization of these advanced platforms, ensuring that cutting-edge laboratory discoveries rapidly transition into clinically available products that address unmet medical needs.

MARKET RESTRAINTS

Complex approval processes for ATMPs delay market entry and increase development costs.

The rigorous and often prolonged regulatory approval landscape in the region acts as a limitation on the rapid commercialization of products within the Europe tissue engineering market. The classification of many tissue-engineered constructs as Advanced Therapy Medicinal Products under the jurisdiction of the European Medicines Agency necessitates extensive preclinical and clinical testing to demonstrate safety and efficacy before market entry. This process involves multiple phases of clinical trials that can span several years and require substantial financial investment, creating a high barrier to entry for smaller biotechnology firms and startups. Regulatory hurdles, including lengthy evaluation periods and frequent requests for supplemental clinical data, often extend the time required to bring advanced therapies to the market after the initial application. The complexity of compliance with Good Manufacturing Practice standards for living cellular products further complicates production scalability, as maintaining cell viability and sterility throughout the manufacturing chain demands specialized infrastructure and highly trained personnel. These regulatory hurdles not only increase the overall cost of product development but also delay patient access to potentially life-saving therapies. Consequently, some innovators may choose to launch their products in regions with more streamlined approval pathways first. This trend slows the introduction of novel tissue engineering solutions in Europe and limits immediate treatment availability for patients.

High manufacturing costs and a lack of harmonized payment models restrict patient access.

Exorbitant production costs coupled with inconsistent reimbursement frameworks are a major hurdle to the widespread adoption of tissue engineering therapies across the region, which in turn negatively impacts the growth of the Europe tissue engineering market. The manufacturing of tissue-engineered products involves sophisticated processes such as cell isolation, expansion, and seeding onto scaffolds under strictly controlled conditions, all of which contribute to significantly higher price points compared to conventional medical devices or pharmaceuticals. The high cost associated with advanced regenerative treatments poses a significant financial challenge for national healthcare systems and insurance providers, potentially limiting patient access to these life-changing therapies. Many European countries lack standardized reimbursement policies for these innovative treatments, leading to fragmented access where patients in certain nations may receive coverage while those in neighboring states face out-of-pocket expenses that are prohibitively expensive. The Health Technology Assessment bodies in various member states often struggle to evaluate the long-term cost-effectiveness of these therapies due to limited real-world evidence and the novelty of the interventions. This uncertainty discourages payers from committing to broad reimbursement schemes, thereby restricting market penetration. Furthermore, the absence of harmonized pricing strategies across the European Union creates market inefficiencies and hampers the ability of manufacturers to achieve economies of scale. Reimbursement models must evolve to recognize the long-term societal benefits of reduced chronic care needs and improved patient productivity. Until this happens, high upfront costs will continue to limit the accessibility of tissue engineering solutions to a broader patient population.

MARKET OPPORTUNITIES

Tailored implants based on genetic profiling and anatomical imaging enhance clinical efficacy.

The convergence of tissue engineering with personalized medicine creates a potential opportunity for the European tissue engineering market. This integration enables the creation of patient-specific implants tailored to individual anatomical and biological profiles. Advances in medical imaging and computational modeling now allow clinicians to design scaffolds that precisely match the defect geometry of a patient, while genetic profiling facilitates the selection of optimal cell sources to minimize immune rejection. This customization enhances clinical outcomes and reduces recovery times, making regenerative therapies more attractive to both surgeons and healthcare payers. The rise of biobanking initiatives across Europe provides a readily available reservoir of characterized cell lines that can be matched to patients based on immunological compatibility, further streamlining the production of autologous and allogeneic constructs. Additionally, the development of point-of-care manufacturing systems allows hospitals to produce tissue-engineered products on site, reducing logistics costs and preserving cell viability. This decentralization of production aligns with the European push towards localized healthcare solutions and resilience. The market is poised for significant expansion as regulatory pathways adapt to these personalized approaches. This shift brings hope to patients with complex injuries or rare conditions, filling a gap that standard products cannot.

Organ-on-chip systems and 3D printed tissues revolutionize toxicity screening and therapeutic fabrication.

The emergence of 3D bioprinting and organ-on-chip technologies offers a lucrative opening for the expansion of the European tissue engineering market. These technologies are revolutionizing both therapeutic applications and drug development pipelines. 3D bioprinting enables the layer-by-layer fabrication of complex tissue structures with precise spatial arrangement of cells and biomaterials, opening new frontiers in the regeneration of vascularized tissues and multi-layered skin grafts. Simultaneously, organ-on-chip platforms utilize microfluidic devices lined with human cells to mimic the physiological functions of entire organs, providing highly predictive models for toxicity testing and efficacy screening. The pharmaceutical industry in Europe increasingly relies on these human-relevant models to replace animal testing, adhering to the EU mandate to reduce animal experimentation while accelerating the drug discovery process. This shift creates a robust demand for high-quality tissue-engineered constructs that can serve as reliable testing substrates. Furthermore, the ability to print functional tissue patches for cardiac or hepatic repair moves the field closer to solving the critical shortage of donor organs. Advancing technology and faster printing speeds are set to make advanced therapies more affordable. This shift will broaden accessibility and solidify Europe’s position as a global leader in regenerative manufacturing.

MARKET CHALLENGES

Inability to replicate complex vascular networks limits the size and viability of engineered organs.

Technical difficulty associated with achieving adequate vascularization within thick or complex engineered tissue constructs remains one of the most persistent challenges to the Europe tissue engineering market. Without a functional blood supply, cells in the interior of large tissue implants suffer from hypoxia and nutrient deprivation, leading to necrosis and graft failure. Despite significant research efforts, replicating the intricate hierarchy of capillaries, arterioles, and venules found in native tissues remains an elusive goal for many bioengineers. Current strategies, such as prevascularization of scaffolds or the incorporation of angiogenic growth factors, have shown promise in preclinical models but often fail to translate consistently into human clinical settings due to the dynamic nature of human physiology. The lack of standardized protocols for inducing rapid and stable vessel formation hinders the scalability of these technologies for widespread clinical use. Moreover, the interaction between engineered vessels and the host circulatory system involves complex immunological and hemodynamic factors that are not yet fully understood. Tissue engineering is largely limited to thin or avascular tissues until we can reliably vascularize thick constructs. Therefore, regenerating complex, vascularized organs like the heart, liver, or kidney remains out of reach.

Public concern over stem cell sources and genetic manipulation influences policy and funding.

Ethical controversies surrounding the source of cells used in tissue engineering products pose a significant obstacle to acceptance and regulatory stability within the European tissue engineering market. The use of embryonic stem cells, although potent in their differentiation capacity, continues to evoke moral objections from various segments of society and religious groups, leading to restrictive policies in certain member states. While induced pluripotent stem cells offer an ethically less contentious alternative, concerns regarding genetic stability and tumorigenicity persist among clinicians and regulators. The skepticism can delay the approval of novel therapies and dampen investor confidence, as companies fear reputational risks or future regulatory reversals. Additionally, the procurement of adult stem cells from donors raises issues related to informed consent and equitable compensation, particularly when commercial products are developed from donated biological materials. The lack of harmonized ethical guidelines across the European Union creates a fragmented landscape where a therapy approved in one country might face bans or severe restrictions in another. Addressing these ethical dimensions requires transparent communication, robust governance frameworks, and active engagement with patient advocacy groups to build trust and ensure that the deployment of tissue engineering technologies aligns with societal values and moral expectations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End-User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | AlloSource, Integra LifeSciences Corporation, Zimmer Biomet Holdings Inc., MIMEDX Group, Inc., Organogenesis Holdings Inc., Medtronic plc, Smith+Nephew, Tissue Regenix, VIVEX Biologics, Inc., Stryker, BioTissue, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The scaffolds segment led the Europe tissue engineering market by occupying a 58.9% share in 2025. This leading position of the segment is driven by the fundamental role scaffolds play as the structural backbone for cell attachment, proliferation, and differentiation in regenerative therapies. Unlike tissue grafts, which are limited by donor availability, scaffolds can be engineered synthetically or derived from natural sources to meet specific clinical requirements, offering unlimited scalability. The top spot of the scaffolds segment is heavily supported by the extensive adoption of synthetic polymers, which offer precise control over mechanical properties and degradation rates. Synthetic materials such as polylactic acid and polyglycolic acid allow engineers to tailor the scaffold architecture to match the specific load-bearing requirements of bone or cartilage defects. The ability to integrate bioactive molecules into these synthetic matrices further enhances their osteoinductive potential, making them superior to traditional grafts in treating critical-size defects. Furthermore, advancements in electrospinning and 3D printing technologies have enabled the production of nanofibrous scaffolds that closely mimic the native extracellular matrix, thereby accelerating cell infiltration. The technological maturity ensures that synthetic scaffolds remain the preferred choice for surgeons dealing with complex orthopedic and craniofacial repairs across the continent. While synthetic options are prevalent, the integration of natural polymers like collagen and hyaluronic acid into scaffold formulations significantly bolsters the market share of this segment by providing superior biocompatibility. Natural scaffolds leverage the inherent biological signals present in proteins to guide tissue regeneration without eliciting strong immune responses, a critical advantage over some synthetic alternatives. The standardization of extraction and purification processes for these natural materials within the European Union ensures consistent quality and safety, addressing previous concerns regarding batch-to-batch variability. Regulatory bodies have streamlined the approval pathways for well-characterized natural scaffolds, reducing the time to market for new products. Additionally, the combination of natural and synthetic components to create hybrid scaffolds offers a balanced approach that maximizes both mechanical strength and biological activity.

The Tissue Grafts segment, particularly allografts, is anticipated to witness the fastest CAGR of 9.8% between 2026 and 2034, owing to the increasing acceptance of processed human donor tissues as a viable alternative to autografts, which require a second surgical site, and xenografts, which face religious and immunological barriers. The main reason for this segment is the clinical imperative to eliminate donor site morbidity associated with autograft harvesting. Autografts, while considered the gold standard, necessitate a secondary surgical procedure to harvest tissue from the patient, leading to increased pain, infection risk, and prolonged hospital stays. According to studies, avoiding donor site complications reduces overall surgical time by several minutes per procedure and decreases postoperative analgesic consumption. This efficiency is highly valued in the context of European healthcare systems striving to optimize operating room throughput and reduce costs. Processed allografts provide an immediate off-the-shelf solution that eliminates the need for harvesting while offering sufficient structural integrity for many applications. The development of advanced processing techniques such as freeze drying and gamma irradiation has significantly improved the safety profile of allografts by effectively neutralizing pathogens without compromising mechanical strength. Consequently, surgeons are increasingly opting for allografts in spinal fusion and sports medicine procedures. The expansion of robust tissue banking networks across Europe serves as a critical driver for the rapid ascent of the tissue grafts segment. Modern tissue banks have implemented rigorous screening and validation protocols that ensure the safety and efficacy of donated tissues, thereby increasing surgeon and patient confidence. These facilities utilize state of the art preservation methods that extend the shelf life of grafts while maintaining their biological properties, allowing for wider distribution and availability. The harmonization of regulatory standards under the European Union Tissues and Cells Directive has further streamlined the cross-border exchange of tissues, ensuring that patients in smaller nations have access to the same quality of grafts as those in larger markets. Additionally, the introduction of decellularized allografts, which remove cellular components to minimize immunogenicity while preserving the extracellular matrix, has expanded the applicability of these grafts to a wider demographic, including immunocompromised patients.

By Application Insights

In 2025, the orthopedic application segment was the largest segment in the European market and captured a share of 42.8%. This growth of the segment is attributed to the high prevalence of musculoskeletal disorders, an aging population prone to joint degeneration, and the widespread adoption of tissue-engineered solutions for bone and cartilage repair. The overwhelming dominance of the orthopedic segment is directly correlated with the escalating burden of osteoarthritis across the European demographic. As life expectancy increases, the wear and tear on weight-bearing joints intensifies, creating a massive demand for effective restoration strategies beyond simple pain management. The epidemic drives the utilization of tissue-engineered cartilage implants and bone void fillers that facilitate biological healing rather than mechanical replacement alone. Traditional metal implants often have limited lifespans and may require revision surgeries, whereas tissue engineering offers the potential for durable biological integration. Furthermore, the rising incidence of sports-related injuries among the younger population contributes to the demand for meniscus repair and ligament reconstruction using engineered grafts. The dual pressure from an aging populace and an active younger generation solidifies orthopedics as the cornerstone of the tissue engineering market. Also supporting this segment is the widespread integration of advanced bone graft substitutes in spinal fusion surgeries. Spinal disorders such as degenerative disc disease and scoliosis require robust fusion masses to stabilize the vertebral column, and tissue-engineered bone grafts have become the preferred alternative to iliac crest autografts. These materials eliminate the pain and complications associated with harvesting bone from the patient's hip while providing osteoconductive scaffolds that support new bone growth. The development of injectable bone cements and 3D printed porous titanium cages coated with bioactive factors has further revolutionized spinal care, allowing for minimally invasive approaches that reduce recovery times. Reimbursement policies in major European markets have evolved to cover these advanced graft materials, recognizing their cost-effectiveness in reducing revision rates and hospital stays. This seamless integration of tissue engineering into routine spinal practices ensures that the orthopedic segment maintains its substantial market share and continues to drive innovation in regenerative musculoskeletal care.

The dermatology application segment is likely to experience the fastest CAGR of 11.2% over the forecast period due to the rising prevalence of chronic wounds, increasing burn incidents, and the burgeoning demand for aesthetic and reconstructive skin solutions. The main pillar of the dermatology segment is the alarming rise in chronic non-healing wounds, particularly diabetic foot ulcers and venous leg ulcers, across the European population. The diabetes epidemic has resulted in a surge of lower extremity complications that often resist conventional dressings and require advanced regenerative interventions to prevent amputation. Traditional care methods fail in a notable portion of these cases, creating a critical need for tissue-engineered skin substitutes that can actively promote granulation and re-epithelialization. These bioengineered constructs provide a living matrix of cells and growth factors that jumpstart the healing process in stalled wounds. Furthermore, the aging population is more susceptible to venous insufficiency, leading to a higher incidence of leg ulcers that benefit from similar regenerative therapies. Healthcare systems are increasingly recognizing the long-term cost savings of preventing amputations through early intervention with advanced skin grafts. This urgent clinical need, combined with favorable reimbursement trends for chronic wound care in countries like France and Germany, positions dermatology as the most rapidly expanding application area in the tissue engineering landscape. Rapid advancements in burn care technologies and the expanding scope of aesthetic reconstructive surgery serve as a second major catalyst for the dermatology segment. Severe burns result in the loss of large surface areas of skin, necessitating immediate coverage to prevent infection and fluid loss, a challenge that tissue-engineered skin grafts address effectively. Engineered epidermal and dermal substitutes allow for the coverage of extensive burn wounds using a small biopsy of the patient's own skin, which is then expanded in the laboratory. This capability is crucial when donor sites are limited. Simultaneously, the aesthetic medicine sector is driving demand for tissue-engineered solutions for scar revision and soft tissue augmentation. The ability of these products to improve cosmetic outcomes and restore texture makes them highly desirable. Moreover, the regulatory approval of novel spray-on skin cell technologies in several European jurisdictions has opened new avenues for rapid wound closure. This convergence of life-saving burn care and high-value aesthetic applications ensures that the dermatology segment will outpace other sectors in growth rate.

By End User Insights

The Hospitals and Ambulatory Surgical Centers (ASCs) segments collectively dominated the Europe tissue engineering market and accounted for a substantial share in 2025. This prominence is due to the concentration of complex surgical procedures, the availability of specialized infrastructure, and the presence of multidisciplinary teams required for administering advanced regenerative therapies. A key force behind the hospitals and ASCs is largely driven by their role as the primary venues for performing complex surgical interventions that necessitate tissue engineering products. Procedures such as spinal fusions, joint replacements, and extensive burn reconstructions require sterile operating environments, advanced imaging, and immediate postoperative care that only hospital settings can provide. These institutions possess the necessary capital equipment, such as 3D bioprinters and cell processing units, which are essential for the intraoperative preparation and application of certain tissue-engineered constructs. Furthermore, hospitals serve as the central hubs for trauma care, managing acute injuries from accidents and sports that often require immediate grafting or scaffold implantation. A study indicates that trauma centers in major European cities handle millions of cases annually, many of which involve soft tissue or bone defects amenable to regenerative treatment. The integration of tissue engineering into standard surgical protocols within these facilities ensures a steady and high-volume demand. Additionally, the presence of teaching hospitals fosters the adoption of innovative techniques as surgeons train the next generation on the latest regenerative technologies, further cementing the dominance of this end-user segment. The dominance of hospitals and ASCs is further reinforced by their capacity to deploy specialized multidisciplinary teams capable of managing the complexities of tissue engineering therapies. Successful outcomes in regenerative medicine often depend on the coordinated efforts of surgeons, pathologists, radiologists, and rehabilitation specialists, a resource model that is intrinsic to hospital operations. These institutions also maintain the stringent cold chain logistics and storage facilities required for living cellular products and sensitive biomaterials, ensuring product viability from delivery to implantation. The European Association of Hospital Pharmacists emphasizes that the handling of Advanced Therapy Medicinal Products requires specialized training and infrastructure that smaller clinics often lack. Moreover, hospitals are better positioned to navigate the regulatory and reimbursement landscapes, possessing dedicated administrative departments to manage the documentation and billing for high-cost regenerative treatments. This operational readiness allows hospitals to adopt new technologies faster than other settings.

The specialty clinics segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 10.5% from 2026 to 2034. This acceleration of the segment is fueled by the shift towards outpatient care, the rise of dedicated aesthetic and orthopedic clinics, and the increasing availability of minimally invasive regenerative procedures. The rapid expansion of specialty clinics is primarily driven by the broader healthcare trend towards shifting complex procedures from inpatient hospital settings to outpatient environments to reduce costs and improve patient convenience. Minimally invasive tissue engineering applications, such as injectable fillers for osteoarthritis or small-scale skin grafts for chronic wounds, can now be safely performed in clinic settings without the need for overnight hospitalization. Specialty clinics offer shorter wait times and personalized care experiences, which are increasingly preferred by patients for elective and semi-elective procedures. The cost efficiency of performing these treatments in clinics rather than hospitals is substantial, with studies showing a reduction in procedural costs. This economic advantage encourages insurance providers and national health systems to refer patients to accredited specialty centers for appropriate tissue engineering interventions. Furthermore, the development of point-of-care devices that allow for the rapid preparation of autologous concentrates and scaffolds within the clinic has empowered these facilities to offer advanced regenerative services independently. Research notes that the adoption of clinic-based injection therapies for joint repair has surged, signaling a structural shift in where tissue engineering is delivered. The proliferation of private specialty clinics focused on aesthetic medicine and sports rehabilitation serves as a second potent driver for the growth of this segment. The booming aesthetic industry in Europe has led to a surge in clinics offering advanced skin rejuvenation, hair restoration, and contouring procedures that utilize tissue-engineered products like platelet-rich plasma scaffolds and dermal fillers. Moreover, the rise of specialized sports medicine clinics catering to athletes and active individuals has increased the demand for rapid recovery solutions such as cartilage repair patches and tendon grafts. These clinics often operate on a cash pay or private insurance model, allowing for quicker adoption of innovative and premium-priced regenerative technologies without the delays associated with public hospital procurement. The European Federation of Sports Medicine Associations highlights that private sports clinics are increasingly integrating biologics into their treatment protocols to ensure faster return to play for patients. The agility of these private entities to invest in new technologies and market them directly to consumers accelerates the penetration of tissue engineering products. This dynamic environment, characterized by high patient volumes and a focus on cutting-edge outcomes, ensures that specialty clinics will continue to outpace traditional hospital settings in growth rate.

COUNTRY LEVEL ANALYSIS

Germany Tissue Engineering Market Analysis

Germany was the top performer in the Europe tissue engineering market and occupied a share of 24.7% in 2025 because of its world-class biomedical research infrastructure, robust manufacturing base, and a healthcare system that prioritizes innovation and high-quality patient care. A dynamic infrastructure of research institutions and biotech clusters actively fuels Germany’s dominance in regenerative medicine research. The country hosts renowned organizations such as the Max Planck Institute and the Fraunhofer Society, which are at the forefront of developing novel biomaterials and cell therapy protocols. The financial backing enables the translation of basic research into commercial products at a pace unmatched by many neighbors. Furthermore, Germany possesses a strong medical device manufacturing sector, with companies specializing in orthopedic implants and surgical tools seamlessly integrating tissue engineering components into their portfolios. The presence of major industry players facilitates rapid clinical adoption and scaling of production. The German healthcare system, characterized by statutory health insurance that covers a wide range of advanced therapies, ensures broad patient access to regenerative treatments. This combination of scientific excellence, industrial capacity, and supportive reimbursement policies solidifies Germany's position as the primary engine of the European tissue engineering market.

United Kingdom Tissue Engineering Market Analysis

The United Kingdom was the next prominent country in the regional market by capturing a 18.5% share in 2025. This expansion of the UK market is driven by its pioneering regulatory framework, strong academic heritage, and concentrated investment in the cell and gene therapy sectors. The competitive advantage of the UK life sciences sector is largely derived from its proactive regulatory environment and strategic focus on advanced therapies. Following its regulatory independence, the Medicines and Healthcare products Regulatory Agency has established streamlined pathways for the approval of innovative tissue engineering products, often acting faster than broader European mechanisms. The country is home to the Cell and Gene Therapy Catapult, a state of the art center that supports the translation of laboratory discoveries into manufacturing-ready processes, bridging the gap between academia and industry. London and Cambridge serve as global hubs for biotech innovation, hosting a dense network of universities and spin-out companies dedicated to tissue engineering. The National Health Service plays a critical role by participating in early adoption programs and clinical trials that validate the efficacy of new therapies. Despite economic fluctuations, the UK's commitment to maintaining its status as a global science superpower ensures sustained growth and leadership in the tissue engineering domain.

France Tissue Engineering Market Analysis

France maintains a significant presence in the Europe tissue engineering market owing to strong government initiatives, a centralized healthcare system, and a growing focus on biotherapeutics and medical biotechnology. Also, France's market strength is underpinned by robust government support and strategic national plans aimed at revitalizing the biohealth sector. The "France 2030" investment plan has earmarked billions of euros specifically for health innovation, including significant grants for tissue engineering and regenerative medicine projects. The country benefits from a centralized healthcare system that facilitates the uniform adoption of new technologies across its network of university hospitals. These centers of excellence serve as key sites for clinical trials and the implementation of advanced regenerative therapies. France also boasts a strong tradition in dermatology and burn care, driving high demand for skin tissue engineering products. The French National Authority for Health has been progressive in evaluating and reimbursing innovative therapies, providing a clear pathway for market entry. This supportive policy landscape, combined with a large patient population and high healthcare spending, ensures that France remains a critical pillar of the European tissue engineering market.

Italy Tissue Engineering Market Analysis

Italy witnessed a consistent growth in the European market due to a strong tradition in medical manufacturing, a high prevalence of age-related conditions, and increasing investment in regenerative research. Its significant market presence is further supported by its formidable medical device industry and the pressing demographic need for solutions to age-related degenerative diseases. The country is a leading manufacturer of orthopedic and dental implants in Europe, and Italian companies are increasingly integrating tissue engineering technologies into their product lines to maintain a competitive advantage. The aging population in Italy creates a substantial burden of osteoarthritis and cardiovascular diseases, fueling the demand for tissue-engineered grafts and scaffolds. The Italian National Health Service supports the adoption of these technologies through specific regional funding programs that encourage innovation in hospital care. Furthermore, Italy has a rich history of stem cell research, with several renowned institutes contributing to global advancements in the field. The Italian Medicines Agency has worked to align its regulatory processes with European standards while maintaining flexibility for compassionate use of experimental therapies. This blend of industrial capability, demographic necessity, and evolving regulatory support positions Italy as a key growth market in the European landscape.

Switzerland Tissue Engineering Market Analysis

Switzerland is anticipated to expand notably in the European market from 2026 to 2034, owing to its high healthcare expenditure, precision engineering capabilities, and status as a global hub for pharmaceutical and biotech headquarters. Despite its smaller population, Switzerland punches above its weight in the tissue engineering market due to its unparalleled wealth, advanced healthcare infrastructure, and concentration of global life sciences corporations. The country is home to numerous multinational pharmaceutical and biotech giants that invest heavily in R&D for regenerative medicines. Switzerland boasts one of the highest per capita healthcare expenditures in the world, which facilitates the early adoption of premium-priced tissue engineering therapies. The regulatory environment, governed by Swissmedic, is known for its rigor and efficiency, attracting companies seeking to launch high-quality products. The country also hosts prestigious research institutions like ETH Zurich that are leaders in biomaterials and 3D bioprinting research. This intense focus on innovation, coupled with a wealthy patient base willing to access cutting-edge treatments, ensures that Switzerland remains a disproportionately influential and lucrative market within the European tissue engineering sector.

COMPETITIVE LANDSCAPE

The competition in the Europe tissue engineering market is characterized by intense rivalry among established multinational corporations and agile biotechnology startups vying for dominance in specific therapeutic areas. Large medical device companies leverage their extensive distribution networks and financial resources to acquire emerging innovators and integrate novel regenerative technologies into their existing portfolios. This consolidation trend creates high barriers to entry for smaller firms unless they possess highly differentiated intellectual property or breakthrough scientific platforms. The competitive landscape is further complicated by the stringent regulatory requirements of the European Medicines Agency, which demand rigorous clinical evidence before market approval. Companies must therefore invest significantly in research and development to demonstrate safety and efficacy while navigating complex reimbursement pathways across diverse national healthcare systems. Innovation speed and the ability to scale manufacturing processes efficiently are critical differentiators that determine market success. Furthermore, strategic alliances between industry players and academic research centers have become essential for accessing cutting-edge science and accelerating product commercialization. The market remains dynamic with continuous entries of new therapies challenging established standards of care.

KEY MARKET PLAYERS

The leading companies operating in the Europe tissue engineering market include:

- AlloSource

- Integra LifeSciences Corporation

- Zimmer Biomet Holdings Inc

- MIMEDX Group, Inc.

- Organogenesis Holdings Inc

- Medtronic plc

- Smith+Nephew

- Tissue Regenix

- VIVEX Biologics, Inc.

- Stryker

- BioTissue

TOP PLAYERS IN THE MARKET

- Zimmer Biomet stands as a global titan in musculoskeletal healthcare with a profound impact on the European tissue engineering landscape. The company leverages its extensive portfolio of orthopedic implants to integrate advanced biologic solutions that enhance bone and soft tissue regeneration. Their contribution to the global market involves pioneering the use of synthetic scaffolds and demineralized bone matrices that serve as critical components in spinal fusion and joint reconstruction surgeries. Recently, Zimmer Biomet has strengthened its position by expanding its regenerative medicine facilities in Switzerland and Germany to accelerate the production of next-generation graft substitutes. The firm actively collaborates with European research institutions to develop novel bioactive coatings that improve implant osseointegration. These strategic moves ensure their technologies remain at the forefront of clinical practice while addressing the growing demand for durable and biologically active orthopedic solutions across the continent.

- Medtronic plc operates as a leading innovator in medical technology with a significant footprint in the European tissue engineering sector, particularly within spinal and cardiovascular applications. The company contributes globally by developing sophisticated delivery systems and bioactive materials that facilitate complex tissue repair and regeneration. Their recent actions to solidify market presence include the launch of advanced osteobiology platforms designed specifically for minimally invasive spinal procedures in major European hospitals. Medtronic has also invested heavily in expanding its manufacturing capabilities in Ireland and the Netherlands to ensure a robust supply chain for its regenerative products. The firm frequently engages in strategic partnerships with academic centers to validate the clinical efficacy of its engineered tissues through rigorous trials. By focusing on integrating digital surgery tools with biological grafts, Medtronic enhances surgical precision and patient outcomes. These efforts demonstrate their commitment to driving innovation and maintaining leadership in the competitive European regenerative medicine arena.

- Organogenesis Holdings Inc is a specialized biopharmaceutical company that has established itself as a key player in the European market through its focus on advanced wound care and surgical solutions. The company makes a substantial global contribution by providing living cellular constructs that effectively treat chronic wounds such as diabetic foot ulcers and venous leg ulcers. Their recent strategy to strengthen their European position involves securing regulatory approvals for new skin substitute products in key markets like France and the United Kingdom. Organogenesis has also expanded its commercial team across the region to increase awareness and adoption of its regenerative therapies among wound care specialists. The firm continues to invest in clinical research programs within Europe to generate real-world evidence supporting the cost-effectiveness of its products. By maintaining a dedicated focus on hard-to-heal wounds, Organogenesis addresses a critical unmet medical need. Their persistent innovation in cell-based therapy ensures they remain a vital partner for healthcare providers seeking advanced solutions for complex tissue loss.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe tissue engineering market predominantly employ strategic acquisitions and partnerships to expand their product portfolios and geographical reach. Companies frequently acquire innovative startups possessing proprietary biomaterial technologies or unique cell processing platforms to instantly enhance their technical capabilities. Another major strategy involves forming extensive collaborations with academic institutions and research hospitals to accelerate clinical trials and validate the efficacy of new regenerative products. Market participants also focus heavily on expanding manufacturing facilities within the European Union to ensure compliance with strict regulatory standards and secure supply chains. Investment in research and development remains a cornerstone strategy as firms strive to develop next-generation scaffolds and bioinks that offer superior clinical outcomes. Additionally, companies pursue aggressive marketing and educational initiatives to train surgeons on the proper application of complex tissue engineering products. These combined approaches allow industry leaders to navigate the complex regulatory landscape while maintaining a competitive edge in this rapidly evolving sector.

EUROPE TISSUE ENGINEERING MARKET NEWS

- In March 2024, Stryker completed the acquisition of SERF SAS, a French joint replacement company. SERF SAS, based in France, is renowned for inventing the Dual Mobility Cup for hip implants. This acquisition directly strengthens Stryker’s presence in the European orthopaedic market by integrating specialized implant technology that supports long-term tissue and joint stability.

MARKET SEGMENTATION

This research report on the Europe tissue engineering market has been segmented and sub-segmented into the following categories.

By Type

- Scaffolds

- Synthetic

- Natural

- Tissue Grafts

- Autograft

- Allograft

- Xenograft

By Application

- Wound Care

- Orthopedic

- Dermatology

- Dental

- Others

By End-user

- Hospital & ASCs

- Specialty Clinics

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe tissue engineering market?

The Europe tissue engineering market creates scaffolds and stem cell therapies for organ repair. Germany dominates manufacturing; UK leads clinical innovation.

How does the Europe tissue engineering market function?

The Europe tissue engineering market functions via biomaterial scaffolds seeded with patient cells, cultured in bioreactors, then implanted surgically for regeneration.

What drives growth in the Europe tissue engineering market?

Aging populations, chronic diseases, and Horizon Europe funding propel the Europe tissue engineering market. Clinical success stories accelerate regulatory approvals.

Which countries lead the Europe tissue engineering market?

Germany commands the Europe tissue engineering market through biomaterials expertise. UK, France, and Italy follow with stem cell research leadership.

What applications define the Europe tissue engineering market?

Orthopedics, cardiology, and skin & integumentary define the Europe tissue engineering market. Neurology applications emerge rapidly.

What materials shape the Europe tissue engineering market?

Hydrogels, decellularized matrices, and synthetic polymers shape the Europe tissue engineering market, providing biocompatibility and mechanical support.

How does regulation influence the Europe tissue engineering market?

EMA advanced therapy classifications and MDR govern the Europe tissue engineering market, ensuring safety while streamlining innovative approvals.

What trends affect the Europe tissue engineering market?

3D bioprinting, organoids, and iPS cell integration transform the Europe tissue engineering market. Personalized implants gain clinical traction.

What challenges face the Europe tissue engineering market?

Vascularization limits, immune rejection risks, and scale-up manufacturing challenge the Europe tissue engineering market. Clinical trial harmonization progresses.

How has 3D bioprinting impacted the Europe tissue engineering market?

3D bioprinting enables complex geometries in the Europe tissue engineering market, revolutionizing cartilage and skin construct precision.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com