Global Veterinary Healthcare Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report By Animal Type (Livestock Animals and Companion Animals), Product (Pharmaceuticals and Feed Additives) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis from 2025 to 2033

Global Veterinary Healthcare Market Summary

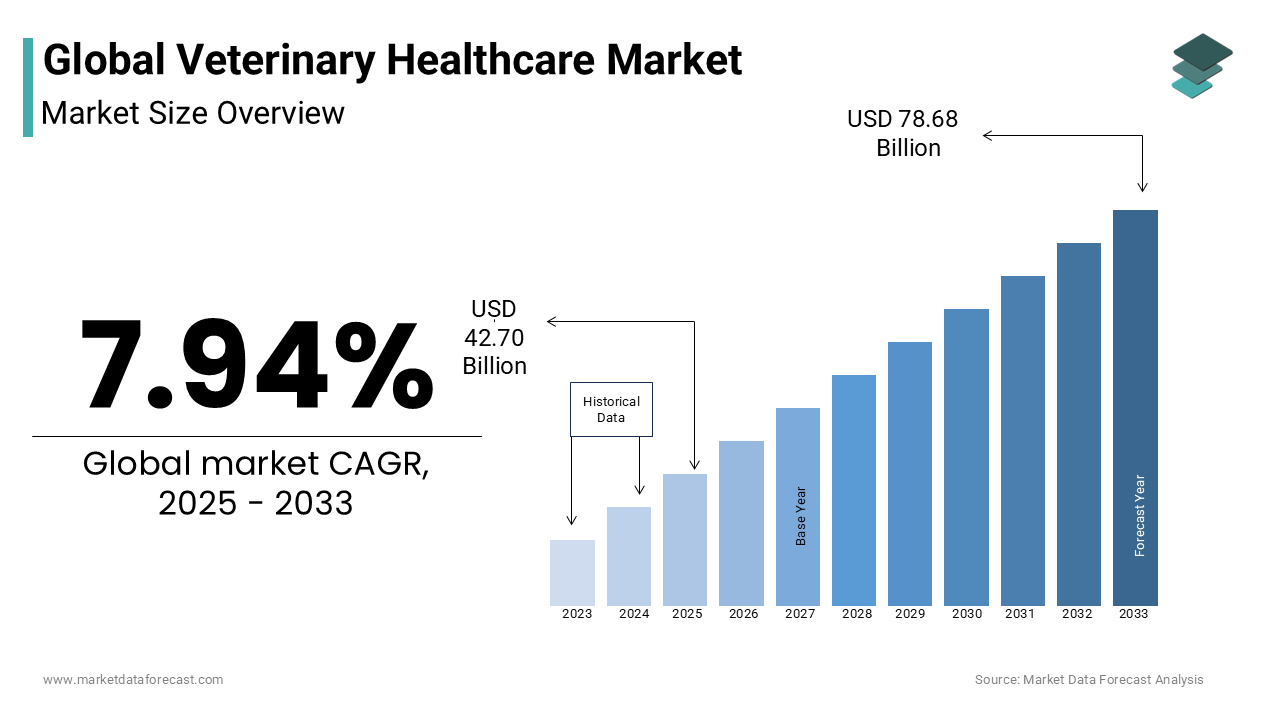

The global veterinary healthcare market was valued at USD 39.56 billion in 2024 and is projected to reach USD 78.68 billion by 2033, growing at a CAGR of 7.94% during the forecast period. The rising prevalence of zoonotic diseases, increasing pet ownership, advancements in veterinary pharmaceuticals, and higher expenditure on animal health worldwide are primarily driving the expansion of the veterinary healthcare market.

Key Market Trends

- Growing pet adoption and humanization of companion animals are fueling healthcare demand.

- Increasing use of preventive care solutions and vaccines in livestock and pets.

- Rising focus on advanced veterinary diagnostics and telemedicine platforms.

- Expanding demand for pharmaceuticals and nutritional products for animal well-being.

Segmental Insights

- Based on animal type, the companion animals segment dominated the global veterinary healthcare market in 2024, supported by increasing pet ownership and rising spending on pet health.

- Based on product, the pharmaceuticals segment held the largest share of the market with 59.3% in 2024, driven by demand for vaccines, parasiticides, and specialty medications.

Regional Insights

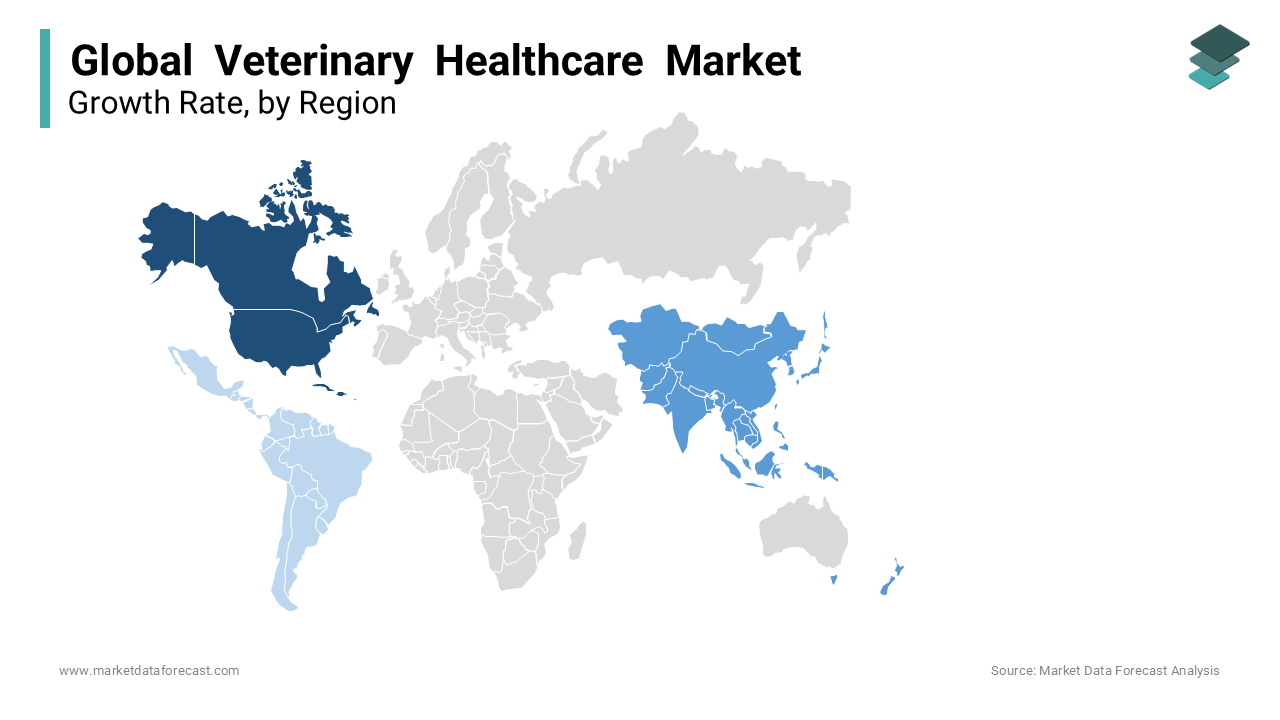

- North America led the global veterinary healthcare market with 38.2% share in 2024, supported by advanced veterinary care infrastructure and high awareness of pet health.

- Asia-Pacific is anticipated to be the fastest-growing region, driven by rising livestock production, increasing urban pet ownership, and growing veterinary investments.

- Europe maintained a significant share due to strong regulatory support and widespread adoption of advanced veterinary practices.

- Latin America shows notable growth potential, supported by expanding livestock industries and higher pet adoption rates.

- Middle East & Africa are witnessing steady growth, backed by government initiatives to improve animal health infrastructure.

Competitive Landscape

Key players in the global veterinary healthcare market include Merck & Co. Inc., Bayer AG, Boehringer Ingelheim International GmbH, Eli Lilly and Company, Ceva Animal Health Inc., Novasep, Novartis AG, Nutreco N.V., Sanofi S.A., Sequent Scientific Ltd., Virbac S.A., and Zoetis S.A.

Global Veterinary Healthcare Market Size

The global veterinary healthcare market is estimated to grow from USD 39.56 billion in 2024 to USD 78.68 billion in 2033, representing a CAGR of 7.94%.

The veterinary healthcare is medical services, pharmaceuticals, diagnostics, surgical interventions, and preventive care dedicated to the well-being of companion animals, livestock, and exotic species. It functions as a parallel infrastructure to human healthcare, integrating clinical expertise, regulatory oversight, and technological innovation to manage diseases that enhance longevity, and improve animal welfare. In the United States, over 70% of households own at least one pet, amounting to more than 218 million dogs, cats, and birds, as documented by the American Pet Products Association in its 2023 survey, reflecting a deepening societal bond between humans and animals.

MARKET DRIVERS

Humanization of Pets and Rising Consumer Willingness to Spend on Animal Health

The anthropomorphization of pets by transforming animals into family members whose medical needs are prioritized akin to human dependents is a major factor amplifying the growth of the veterinary healthcare market. This psychological shift is particularly pronounced in North America and Western Europe, where over 67% of pet owners consider their animals integral to emotional well-being, as reported by the Human-Animal Bond Research Institute. The emotional investment translates into tangible healthcare expenditures, with owners increasingly opting for advanced diagnostics, surgical procedures, and chronic disease management. According to the American Pet Products Association, the average annual veterinary expenditure per dog owner reached $987 in 2023, a 38% increase from 2018, reflecting a willingness to pursue treatments once considered economically unjustifiable. This includes oncology care, where radiation therapy and chemotherapy for pets are now offered at over 150 specialty centers across the U.S., as cataloged by the American College of Veterinary Internal Medicine.

Expansion of Preventive and Diagnostic Veterinary Services

The shift from reactive to preventive veterinary care is fundamentally altering the structure of animal health service delivery, which is additionally fuelling the growth of the veterinary healthcare market. Veterinary clinics are increasingly adopting protocols similar to human preventive medicine, including annual blood panels, dental assessments, and vaccination schedules tailored to breed and lifestyle. As per the American Animal Hospital Association, over 80% of accredited practices now offer comprehensive wellness packages that include thyroid function tests, heartworm screening, and urinalysis for pets over seven years of age. Furthermore, imaging technologies such as digital radiography and ultrasound are becoming standard in general practice, with the Veterinary Information Network noting a 40% increase in diagnostic imaging utilization between 2020 and 2023. Preventive care not only improves animal outcomes but also strengthens client retention and practice revenue, incentivizing clinics to expand service portfolios.

MARKET RESTRAINTS

Shortage of Qualified Veterinary Professionals and Clinical Capacity Constraints

The expansion of veterinary healthcare services is hindering the growth of the veterinary healthcare market. Despite rising pet ownership, the supply of veterinary professionals has not kept pace with demand. As per the American Veterinary Medical Association, there are approximately 1.2 veterinarians per 10,000 pets in the U.S., a ratio that varies significantly by region, with rural areas facing severe shortages. The Association of American Veterinary Medical Colleges reports that U.S. veterinary schools graduate only about 4,000 new doctors annually, insufficient to replace retiring practitioners and meet growing needs. Burnout is widespread, with a 2022 Merck Animal Health study indicating that 80% of veterinarians experience work-related stress, and 14% report suicidal ideation, contributing to early career exits. The shortage also affects specialty services, where board-certified specialists in fields like veterinary oncology and cardiology remain concentrated in urban centers.

Regulatory Fragmentation and Approval Delays for Veterinary Pharmaceuticals

The development and commercialization of veterinary therapeutics are hindered by a complex and fragmented regulatory environment that slows innovation and market entry. Unlike human pharmaceuticals, which benefit from centralized pathways through the FDA’s Center for Drug Evaluation and Research, veterinary drugs are overseen by the FDA’s Center for Veterinary Medicine (CVM), which operates with significantly fewer resources and a more protracted approval timeline. According to the Government Accountability Office, the median review period for a new animal drug application exceeds 42 months, nearly double that of human drug approvals. Additionally, labeling restrictions often prevent extralabel use of approved drugs, even when clinically justified, as mandated by the Animal Medicinal Drug Use Clarification Act. Furthermore, differing regulatory standards across states complicate interstate practice and telemedicine, particularly for prescription issuance. The lack of harmonized data requirements for clinical trials in animals also increases R&D costs. As per the Animal Health Institute, only 45 new animal drug entities were approved between 2010 and 2020, compared to over 400 human drugs in the same period.

MARKET OPPORTUNTIES

Integration of Digital Health Technologies and Telemedicine Platforms

The adoption of digital health solutions to expand access, improve diagnostics, and enhance client engagement in veterinary medicine is expected to substantially elevate the growth of the veterinary healthcare market. Telemedicine, once limited by regulatory barriers, has gained legitimacy following temporary relaxations during the pandemic, with states like California and Texas now permitting remote consultations under defined conditions. These tools enable follow-up evaluations, behavioral counseling, and chronic disease monitoring without requiring physical visits, alleviating clinic congestion. Wearable biosensors for pets, such as collar-based activity and heart rate monitors, are generating continuous health data that can be integrated into electronic medical records. The American Animal Hospital Association notes that over 30% of practices now use remote monitoring devices to track conditions like diabetes and congestive heart failure. Cloud-based practice management systems from firms like Covetrus and Henry Schein are streamlining workflows, inventory tracking, and client communication. The convergence of these technologies is enabling predictive health modeling and personalized care plans, mirroring advancements in human digital health.

Growth in Livestock Health Management Driven by Food Security and Biosecurity Concerns

The intensification of global food production systems is anticipated to boost the growth of the veterinary healthcare market in the following years. In the U.S., the Department of Agriculture reports that over 95% of commercial cattle, swine, and poultry operations implement veterinary-supervised health programs to prevent outbreaks of diseases such as porcine reproductive and respiratory syndrome (PRRS) and avian influenza.

MARKET CHALLENGES

Rising Antimicrobial Resistance and Pressure to Reduce Antibiotic Use in Animals

The veterinary sector faces mounting pressure to curtail antibiotic usage due to the escalating threat of antimicrobial resistance (AMR), which jeopardizes both animal and human health. The Centers for Disease Control and Prevention estimates that over 2.8 million antibiotic-resistant infections occur annually in the U.S., with a significant proportion linked to agricultural antibiotic use. Veterinarians are increasingly required to justify antibiotic prescriptions, and alternatives such as probiotics, phage therapy, and vaccines are still in developmental stages. The World Organisation for Animal Health notes that less than 20% of veterinary practices routinely perform antimicrobial susceptibility testing before prescribing, limiting treatment precision. Additionally, global trade regulations, such as those from the European Union, impose strict residue limits, affecting export eligibility. The One Health initiative, which integrates human, animal, and environmental health, places veterinarians at the frontline of AMR mitigation, demanding a paradigm shift toward stewardship, surveillance, and alternative interventions.

Economic Disparities in Access to Veterinary Care Across Regions and Species

Veterinary healthcare is the unequal access to services, driven by socioeconomic, geographic, and species-based disparities, which also hinders the growth of the veterinary healthcare market. In rural and low-income communities, veterinary clinics are often scarce or nonexistent, leaving pet owners and livestock producers without timely care. This is compounded by the absence of universal insurance or public funding, unlike human healthcare. For livestock, small-scale and subsistence farmers often lack resources for preventive care, increasing disease vulnerability. The uneven distribution of emergency and specialty care further exacerbates inequities, with services like oncology and surgery concentrated in metropolitan areas.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Animal Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leader Profiled | Merck & Co. Inc., Bayer AG, Boehringer Ingelheim International GmbH, Eli Lilly and Company, Ceva Animal Health Inc., Novasep, Novartis AG, Nutreco N.V., Sanofi S.A., Sequent Scientific Ltd., Virbac S.A., Zoetic S.A. |

SEGMENTAL ANALYSIS

By Animal Type Insights

The companion animals segment dominated the global veterinary healthcare market by capturing a dominant share in 2024, due to the deepening emotional integration of pets into household structures has redefined veterinary spending as a non-negotiable aspect of family welfare. This widespread ownership is accompanied by a willingness to invest in advanced medical interventions; the average annual veterinary expenditure per dog owner reached $987 in 2023, a 38% increase from 2018, as documented by the same source. The aging pet population is significantly increasing the demand for chronic disease management and geriatric care. Banfield Pet Hospital’s 2023 State of Pet Health report indicates that nearly 40% of dogs and cats in the U.S. are now classified as senior (aged seven or older), a demographic requiring regular bloodwork, joint therapies, and specialized nutrition. This mirrors human healthcare trends, where preventive screenings and long-term medication regimens are standard.

The livestock animals segment is projected to grow at a CAGR of 6.7% from 2025 to 2033, with escalating concerns over food security and zoonotic disease outbreaks are driving intensified veterinary oversight in animal agriculture. The U.S. Department of Agriculture reports that over 95% of commercial cattle, swine, and poultry operations now operate under veterinary-supervised health protocols to prevent diseases such as avian influenza and bovine respiratory disease.

By Product Insights

The pharmaceuticals segment was the largest by accounting for 59.3% of the veterinary healthcare market share in 2024 with the rising prevalence of chronic and infectious diseases in both companion and livestock animals has intensified the demand for therapeutic interventions. In companion animals, conditions such as diabetes, osteoarthritis, and heart disease are increasingly diagnosed due to improved veterinary diagnostics and longer lifespans.

The feed additives segment is likely to register a CAGR of 7.3% from 2025 to 2033 as the global push to reduce antibiotic use in livestock has accelerated the adoption of alternative growth promoters and health enhancers. In response to antimicrobial resistance (AMR) concerns, regulatory bodies such as the U.S. FDA and the European Medicines Agency have restricted the use of medically important antibiotics for growth promotion. This has created a surge in demand for non-antibiotic feed additives, including probiotics, prebiotics, organic acids, and phytogenics. According to the International Probiotics Association, global sales of probiotic feed additives reached $5.2 billion in 2023, with North America and Europe leading adoption.

REGIONAL ANALYSIS

North America Veterinary Healthcare Market Insights

North America was the largest and held 38.2% of the global veterinary healthcare market share in 2024 with the anchored in high pet ownership rates, advanced veterinary infrastructure, and robust regulatory frameworks. In the United States, over 70% of households own a pet, with annual veterinary expenditures exceeding $35 billion, according to the American Pet Products Association. The presence of major pharmaceutical companies such as Zoetis, Merck Animal Health, and Elanco enables rapid innovation and product commercialization. Additionally, the USDA’s stringent animal health regulations ensure high standards in livestock disease control, particularly for export-oriented agriculture. The integration of telemedicine, digital diagnostics, and pet insurance has further modernized service delivery.

Europe Veterinary Healthcare Market Insights

Europe was positioned second with 29.3% of the global veterinary healthcare market share in 2024. The European Union mandates veterinary oversight for all antibiotic use in livestock, and its ban on growth-promoting antibiotics since 2006 has driven innovation in alternative health solutions. Germany, France, and the UK are leading national markets, with Germany alone spending over €4.2 billion annually on veterinary services, according to the Federation of Veterinarians of Europe. The EU’s Farm to Fork Strategy aims to reduce antimicrobial sales by 50% by 2030, accelerating the adoption of vaccines and feed additives. Additionally, pet humanization trends are rising, with 215 million companion animals across the region, as documented by FEDIAF. These regulatory and cultural dynamics position Europe as a leader in sustainable and ethical veterinary practices.

Asia Pacific Veterinary Healthcare Market Insights

Asia Pacific veterinary healthcare market is likely to witness a significant CAGR during the forecast period owing to the rising disposable incomes, urbanization, and increasing pet ownership in countries like China, India, and South Korea. In parallel, intensification of livestock farming to meet protein demand has increased veterinary oversight in the poultry and swine sectors. However, fragmented regulatory systems and uneven access to veterinary services remain challenges. Japan stands out with a mature market, where pet insurance and geriatric care are well-established.

Latin America Veterinary Healthcare Market Insights

Latin America veterinary healthcare market growth is likely to grow with the growing companion animal sector and a dominant livestock health segment. In urban centers like São Paulo and Mexico City, pet ownership is rising, with increased spending on premium food and medical care. However, economic volatility and limited insurance penetration constrain widespread access.

Middle East & Africa Veterinary Healthcare Market Insights

The Middle East and Africa veterinary healthcare market is growing steadily in the next coming years. The region’s dynamics are shaped by livestock-dependent economies and emerging pet care markets. In sub-Saharan Africa, over 70% of rural households rely on livestock for livelihoods, making veterinary services for food security, as noted by the FAO. Countries like Kenya and Ethiopia are investing in mobile veterinary units and vaccination campaigns to combat diseases such as foot-and-mouth and Rift Valley fever. The Gulf Cooperation Council nations, particularly the UAE and Saudi Arabia, are witnessing rapid growth in companion animal care, driven by expatriate populations and urban affluence. Dubai alone has over 150 veterinary clinics, according to the Emirates Veterinary Association. However, limited regulatory frameworks and uneven professional distribution hinder scalability.

COMPETITIVE LANDSCAPE

Key Market Participants

Companies playing a key role in the global veterinary healthcare market include

- Merck & Co. Inc.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Eli Lilly and Company

- Ceva Animal Health Inc.

- Novasep

- Novartis AG

- Nutreco N.V.

- Sanofi S.A.

- Sequent Scientific Ltd.

- Virbac S.A.

- Zoetic S.A.

The competitive landscape of the veterinary healthcare market is defined by a convergence of scientific innovation, evolving consumer expectations, and global health imperatives. While a few dominant multinational corporations command significant influence, the market is increasingly shaped by niche players specializing in digital diagnostics, alternative therapeutics, and species-specific solutions. Competition is no longer limited to product efficacy or pricing but extends to ecosystem integration, where companies vie to offer end-to-end care platforms that combine pharmaceuticals, monitoring devices, and data analytics. The rise of pet humanization has intensified demand for premium services, pushing firms to differentiate through personalized treatment plans and enhanced client experiences. In the livestock sector, competition is driven by biosecurity capabilities, regulatory compliance, and sustainability credentials, with producers favoring partners who can ensure herd health while meeting export standards. Mergers, acquisitions, and cross-sector collaborations are common as companies seek to expand portfolios and geographic reach.

Top Players in the Veterinary Healthcare Market

Zoetis

Zoetis stands as a global leader in veterinary medicine, operating as the world’s largest animal health company dedicated exclusively to the well-being of animals. The company has pioneered innovations in pharmaceuticals, vaccines, and diagnostics for both companion and food-producing animals, integrating scientific rigor with practical clinical application. Its broad portfolio spans therapeutic areas such as pain management, parasitology, and immunology, supporting veterinarians in delivering advanced care. Zoetis actively collaborates with veterinary institutions, regulatory agencies, and research networks to shape industry standards and accelerate product development. Its global footprint ensures that breakthrough therapies reach diverse markets, from urban pet clinics to large-scale livestock operations by making Zoetis a cornerstone of modern veterinary healthcare advancement.

Elanco Animal Health

Elanco Animal Health has established itself as a transformative force in the veterinary sector by focusing on sustainable, science-driven solutions for livestock and companion animals. The company emphasizes improving animal productivity and health through innovative pharmaceuticals, feed additives, and digital platforms that support precision farming. Elanco’s commitment to reducing antimicrobial use has led to the development of alternative health technologies that align with global food safety goals. It fosters strong partnerships with farmers, veterinarians, and academic institutions to ensure its products meet real-world needs. Through a balanced focus on innovation, ethics, and accessibility, Elanco plays a vital role in shaping the future of animal health worldwide.

Merck Animal Health (a division of Merck & Co.)

Merck Animal Health combines the scientific legacy of a global pharmaceutical leader with a specialized focus on veterinary medicine, which is delivering a comprehensive range of vaccines, parasiticides, and diagnostic solutions. The company is recognized for its contributions to disease prevention, particularly in livestock, where its vaccines protect against economically devastating conditions. It also advances companion animal care through targeted therapies for chronic diseases and behavioral health. Merck Animal Health invests heavily in research collaborations and public-private initiatives to combat zoonotic diseases and antimicrobial resistance. Its educational outreach programs support veterinary professionals in adopting best practices.

Top Strategies Used by Key Market Participants

A primary strategy among leading veterinary healthcare companies is the vertical integration of product development with clinical and digital ecosystems. Firms are no longer confined to manufacturing pharmaceuticals or devices but are expanding into software platforms, telemedicine interfaces, and diagnostic networks that enhance treatment efficacy and client engagement. This integration allows for real-time monitoring, data-driven decision-making, and seamless care coordination, transforming veterinary practice from episodic treatment to continuous health management.

Another key approach is strategic partnerships with academic institutions, government agencies, and agricultural cooperatives to drive innovation and regulatory influence. Alliances also facilitate access to emerging markets and strengthen credibility in both companion and livestock sectors.

In addition, the expansion into preventive and wellness-centric product lines will also help the companies to expand their base. Companies are shifting focus from reactive treatments to proactive health solutions, including nutraceuticals, early-detection diagnostics, and life-stage-specific care regimens. This not only meets rising consumer demand for holistic pet care but also builds long-term brand loyalty and recurring revenue streams through subscription-based models and bundled health plans.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Zoetis launched a digital health platform integrating AI-powered diagnostic support for veterinarians by enabling faster interpretation of lab results and imaging studies across companion animal practices in North America and Europe.

- In July 2023, Elanco Animal Health partnered with a leading agricultural technology firm to develop a wearable sensor system for cattle, which is designed to monitor vital signs and detect early signs of illness in dairy herds.

- In October 2023, Merck Animal Health introduced a new vaccine for swine influenza with broader strain coverage by enhancing disease prevention capabilities for pork producers across the United States and Southeast Asia.

- In January 2024, Boehringer Ingelheim acquired a biotech startup specializing in monoclonal antibody therapies for canine cancer, which is reinforcing its position in advanced companion animal oncology.

- In May 2024, IDEXX Laboratories expanded its reference lab network into India and Nigeria by strengthening diagnostic accessibility and supporting veterinary practices in emerging markets.

MARKET SEGMENTATION

This research report on the global veterinary healthcare market has been segmented and sub-segmented based on the product, animal type, and region.

By Product

- Pharmaceuticals

- Vaccines

- Antibiotics

- Parasiticides

- Others

- Feed Additives

- Medical Feed Additives

- Nutritional Feed Additives

By Animal Type

- Livestock Animals

- Cattles

- Swine

- Sheep

- Poultry

- Aquatic

- Others

- Companion Animals

- Cats

- Dogs

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa (MEA)

Frequently Asked Questions

What are the factors fueling the veterinary healthcare market?

Increased pet ownership across the world and growing incidence of animal diseases are primarily promoting the veterinary healthcare market growth.

Which region accounted for the largest share of the market in 2023?

Geographically, the North American region held the major share of the market in 2023.

Who are the major participants in the veterinary healthcare market?

Merck & Co., Inc., Bayer AG, Boehringer Ingelheim GmbH, Cargill, Inc., Ceva Santé Animale, Novasep, Eli Lilly and Company, Koninklijke DSM N.V., Novartis AG, Nutreco N.V., Sanofi S.A., Sequent Scientific Ltd., Virbac S.A., Vétoquinol S.A., and Zoetis Inc. are some of the noteworthy companies in the veterinary healthcare market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com